Global Brake Components for Automobile Market - Size and Forecast Analysis, 2021-2035

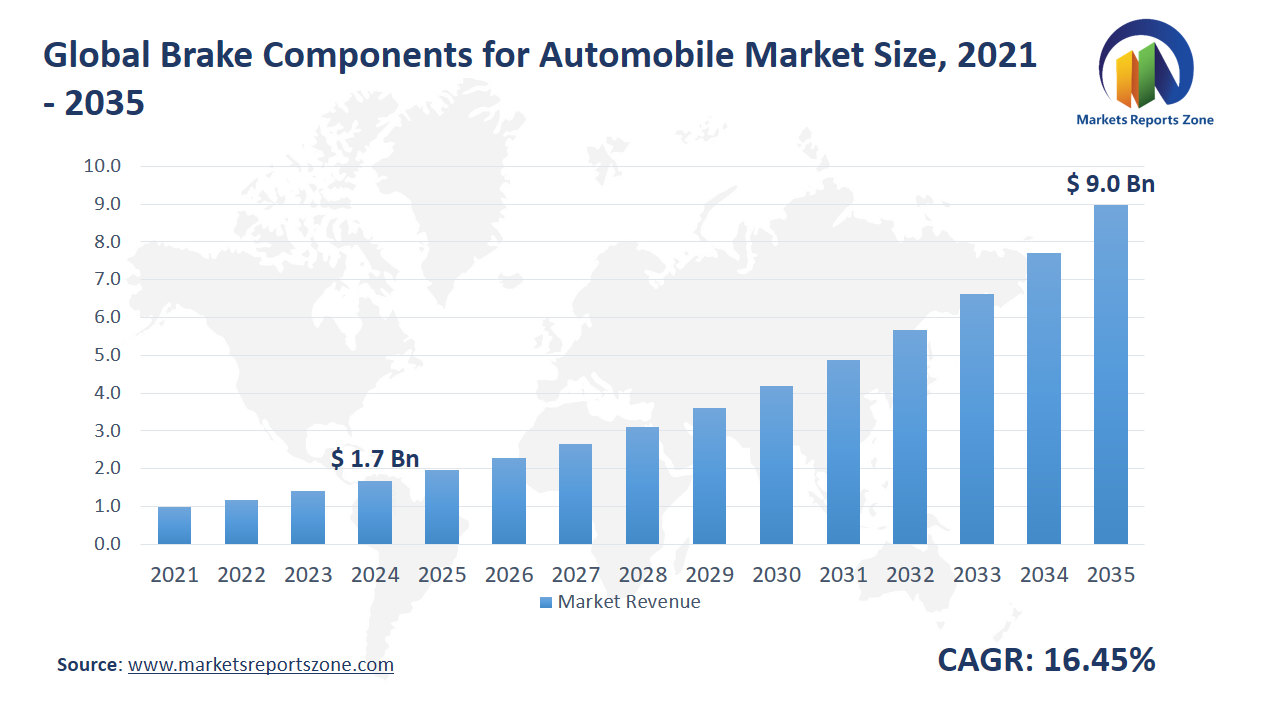

Global Brake Components for Automobile Market Size is expected to reach USD 9 Billion by 2035 from USD 1.68 Billion in 2024, with a CAGR of around 16.45% between 2024 and 2035. The global brake components for automobile market has been driven by rising vehicle safety awareness and increased automotive production. Brake upgrades have been demanded by both new buyers and used vehicle owners, especially in urban areas with heavy traffic. Advanced braking technologies like ABS and EBD have been widely adopted, improving control and reducing accidents. However, the market has been restrained by fluctuating raw material prices, which have impacted the cost of key components like rotors and pads. Manufacturers have faced challenges in maintaining margins while ensuring performance standards. Still, opportunities have emerged with the growth of electric vehicles, which require specialized brake systems such as regenerative braking and low-noise components. Additionally, rising demand for performance vehicles has opened space for high-end brake systems, including carbon-ceramic discs and ventilated calipers. For example, in cities like Munich and Seoul, sports car owners have upgraded to track-ready braking kits for enhanced control and durability. Ride-hailing fleets in Southeast Asia have also begun using longer-lasting brake pads to reduce downtime and maintenance costs. The market has continued to shift toward innovation, with lightweight materials and smart braking sensors being gradually introduced to meet both safety expectations and sustainability goals.

Driver: Safety Awareness Boosts Brake Innovation

Rising awareness around vehicle safety has played a major role in driving demand for advanced brake components. As road traffic increases and driving conditions become more unpredictable, both consumers and manufacturers have placed greater emphasis on reliable braking systems. Drivers today are more informed about the importance of quick stopping power, reduced braking distance, and stable control under emergency conditions. This shift has pushed automakers to equip even entry-level vehicles with features like anti-lock braking systems and electronic brake-force distribution. In regions with high accident rates, these features have become major selling points. For instance, in countries like South Africa and Indonesia, consumer preference has shifted toward vehicles offering enhanced safety features, including better brake performance. Commercial vehicle operators have also taken notice, upgrading their fleets with more responsive braking systems to reduce liability and improve driver confidence. Urban delivery vans in busy cities like Cairo and Manila have begun using disc brakes over drum brakes for improved stopping efficiency in dense traffic. Brake component makers have responded with innovations in pad materials, rotor design, and system integration. With rising public demand and regulatory pressure, safety has become not just a feature but a fundamental expectation in every modern vehicle.

Key Insights:

- Over 80% of newly manufactured passenger cars globally were equipped with anti-lock braking systems by the end of 2023.

- A major automotive group invested $500 million in upgrading brake system manufacturing plants across North America and Europe.

- More than 150 million brake pad units were produced in Asia-Pacific in 2022, serving both OEM and aftermarket demand.

- Disc brakes had a penetration rate of over 70% in the global light commercial vehicle segment, replacing drum brakes in newer models.

- Government safety mandates in Europe led to an increase in electronic stability and brake assist systems adoption across 60% of new vehicles.

- Electric vehicle manufacturers integrated regenerative braking systems in over 90% of their models sold in 2023.

- Heavy commercial vehicle fleets in the Middle East reported a 40% upgrade rate to high-performance brake components for desert driving conditions.

- A leading brake system supplier shipped over 25,000 tons of brake rotors and calipers globally through OEM contracts in 2023.

Segment Analysis:

The brake components market has developed across various segments driven by vehicle performance needs and safety regulations. Brake rotors have remained critical for efficient stopping power and are widely used in both passenger and commercial vehicles. Slotted and ventilated rotors have been preferred in high-performance vehicles to handle heat and reduce fade during repeated braking. Brake boosters have become essential in modern vehicles to reduce pedal effort and improve braking response, particularly in passenger cars and light commercial vehicles used in city driving. Brake pads, one of the most frequently replaced components, have seen rising demand in both OEM and aftermarket sectors. Ceramic and low-metallic pads have gained popularity due to reduced noise and better durability. On the application side, passenger cars continue to lead adoption as safety features like ABS and EBD become standard. Light commercial vehicles have shown increased usage of enhanced brake pads and boosters to support urban logistics and delivery operations. Heavy commercial vehicles and trucks require robust brake rotors and high-friction pads for long-haul stability and performance. For example, logistics fleets in cold-weather regions have switched to corrosion-resistant rotors to handle harsh conditions. These evolving requirements across segments have shaped product innovation and material upgrades across the industry.

Regional Analysis:

The global brake components market shows varying dynamics across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In North America, stringent road safety regulations and a large SUV and pickup segment have increased demand for high-performance rotors and pads. Many suburban families in the U.S. have opted for vehicles equipped with advanced brake boosters for added safety. Europe has focused on eco-friendly materials and noise-reducing technologies in brake pads, particularly in electric and hybrid cars. Scandinavian countries have emphasized winter brake performance, leading to a rise in demand for coated and ventilated rotors. In Asia-Pacific, rapid urbanization and rising vehicle ownership in nations like Indonesia and Vietnam have boosted demand for affordable yet durable brake systems. Smaller city cars and two-seater EVs have driven volume growth in this region. Latin America has seen consistent growth in the aftermarket segment, with countries like Argentina reporting higher sales of semi-metallic pads for older passenger vehicles. Meanwhile, in the Middle East & Africa, brake components built for high heat resistance have been preferred in desert climates. Long-haul trucks traveling across arid regions have required heavy-duty boosters and fade-resistant pads, encouraging localized manufacturing. Each region’s unique driving conditions and regulations continue to shape brake component trends.

Competitive Scenario:

Key players in the global brake components market have continued to evolve through innovation, strategic partnerships, and performance upgrades. Centric Parts and Brake Parts Inc. have expanded their offerings in the aftermarket sector, focusing on long-lasting pads and corrosion-resistant rotors tailored for everyday vehicles. Winhere Brake Parts has scaled up production capacity to meet rising OEM demands, especially in emerging Asian markets. ATTC has developed new formulations in brake disc casting to improve thermal performance. Brembo SpA has launched lightweight carbon-ceramic systems targeted at electric and high-end performance vehicles, aligning with the shift toward sustainable mobility. SGL Group and Surface Transforms Plc have collaborated on advanced carbon composite brake discs used in motorsports and luxury cars. Akebono Brake Corporation has introduced low-dust brake pad technology that enhances cleanliness and comfort, especially for city driving. Fusion Brakes and Sicom have catered to niche segments like racing and aerospace with ultra-lightweight and high-temperature brake components. Rotora and Alcon Components Limited have expanded into aftermarket tuning, offering sport brake kits for off-road and performance vehicles. Bosch Auto Parts continues to lead in brake electronics integration, while NewTek Automotive and Brakes International focus on durable solutions for commercial fleets. Nasco Aircraft Brake also explores cross-industry applications in specialized transport systems.

Brake Components for Automobile Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 1.68 Billion |

| Revenue Forecast in 2035 | USD 9 Billion |

| Growth Rate | CAGR of 16.45% from 2025 to 2035 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2035 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Centric Parts; Brake Parts Inc.; winhere brake parts; ATTC; Brembo SpA; SGL Group; Surface Transforms Plc; Akebono Brake Corporation; Fusion Brakes; Sicom (MS Production); Rotora; Brakes International; Bosch Auto Parts; Nasco Aircraft Brake; NewTek Automotive USA; Alcon Components Limited |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Brake Components for Automobile Market report is segmented as follows:

By Type,

- Brake Rotors

- Brake Boosters

- Brake Pads

By Application,

- Passenger Car (PC)

- Light Commercial Vehicle (LCV)

- Heavy Commercial Vehicle (HCV)

- Truck

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

Key Market Players,

- Centric Parts

- Brake Parts Inc.

- winhere brake parts

- ATTC

- Brembo SpA

- SGL Group

- Surface Transforms Plc

- Akebono Brake Corporation

- Fusion Brakes

- Sicom (MS Production)

- Rotora

- Brakes International

- Bosch Auto Parts

- Nasco Aircraft Brake

- NewTek Automotive USA

- Alcon Components Limited

Frequently Asked Questions

How big is the Brake Components for Automobile market?

Global Brake Components for Automobile Market Size was valued at USD 1.68 Billion in 2024 and is projected to reach at USD 9 Billion in 2035.

What is the Brake Components for Automobile market growth?

Global Brake Components for Automobile Market is expected to grow at a CAGR of around 16.45% during the forecasted year.

Which region has the largest market share in Brake Components for Automobile market?

North America, Asia Pacific and Europe are major regions in the global Brake Components for Automobile Market.

Who are the key players in Brake Components for Automobile market?

Key players analyzed in the global Brake Components for Automobile Market are Centric Parts; Brake Parts Inc.; winhere brake parts; ATTC; Brembo SpA; SGL Group; Surface Transforms Plc; Akebono Brake Corporation; Fusion Brakes; Sicom (MS Production); Rotora; Brakes International; Bosch Auto Parts; Nasco Aircraft Brake; NewTek Automotive USA; Alcon Components Limited and so on.