Global Data Center Blade Server Market, By Form Factor (Half-height Blade Server, Full-height Blade Server, Quarter-height Blade Server), By Channel, By Application, By End-use, and By Region - Trends and Forecast Analysis, 2021-2033

Publish Date: 2025-03-04 | Format: PDF | Category: ICT Media | Pages: 320

The Global Data Center Blade Server Market size was valued at USD 18.56 Billion in 2024 and is projected to reach USD 42.81 Billion by 2033 at a CAGR of around 9.73% between 2024 and 2033. The global data center blade server market is driven by rising cloud adoption and growing demand for energy-efficient solutions. Cloud service providers deploy blade servers to optimize space and power usage. Enterprises shift workloads to hybrid cloud environments, boosting blade server adoption. However, high initial investment acts as a restraint. Businesses hesitate due to expensive hardware and setup costs. Despite this, two major opportunities exist. First, edge computing growth is increasing demand for compact and high-performance blade servers. Telecom companies integrate these servers for low-latency applications like autonomous vehicles and smart cities. Second, AI and big data analytics require high-density computing, creating demand for blade servers with advanced GPU integration.

Financial institutions use them for real-time fraud detection and predictive analytics. Major players continuously innovate to enhance efficiency and processing power. Hyperscalers expand data centers, further driving market growth. Sustainability concerns push manufacturers to develop energy-efficient blade servers. Governments incentivize green IT infrastructure, accelerating adoption. As digital transformation accelerates, demand for high-performance computing increases. The healthcare sector also relies on blade servers for AI-driven diagnostics and patient data management. While cost remains a challenge, advancements in modular server technology reduce expenses over time, making adoption more feasible across industries.

Driver: Cloud Adoption Fueling Blade Server Growth

The rise of cloud computing is driving demand for blade servers in data centers. Businesses are shifting operations to the cloud to improve scalability and efficiency. Blade servers, known for their compact design and high processing power, are essential for cloud infrastructure. Companies like e-commerce giants deploy these servers to handle millions of transactions daily. Streaming platforms use them to deliver seamless video content worldwide. Cloud gaming services rely on them for low-latency gameplay experiences. Startups and enterprises prefer hybrid cloud models, integrating blade servers for workload management.

Government agencies store vast amounts of citizen data on cloud-based blade servers for security and accessibility. Educational institutions run virtual learning platforms efficiently using these servers. Social media companies use them to process and store user-generated content at massive scales. Airlines depend on cloud-powered blade servers for real-time flight scheduling and ticketing systems. Businesses leverage private cloud setups with blade servers for enhanced data security and compliance. The demand is further accelerated by increasing digital services and remote work adoption. As cloud infrastructure expands, blade servers remain a critical component, ensuring speed, reliability, and seamless connectivity across industries. Their role in supporting digital transformation makes them indispensable for modern enterprises.

Key Insights:

- A major telecommunications provider reported a 30% increase in blade server deployments for edge computing initiatives in their annual report.

- Government infrastructure projects allocated $500 million towards data center upgrades, including blade server installations, as per their annual budget.

- An industry association noted a 25% adoption rate of blade servers in financial institutions for high-frequency trading.

- A large cloud service provider's annual report indicated the deployment of several thousand blade server units for their expanded data center footprint.

- The healthcare sector showed a 15% penetration rate of blade servers for managing electronic health records, according to hospital association data.

- A technology hardware company disclosed a 40% rise in blade server shipments to research and development facilities in their annual report.

- Educational institutions reported a 20% increase in blade server usage for high-performance computing clusters in their annual reports.

Segment Analysis:

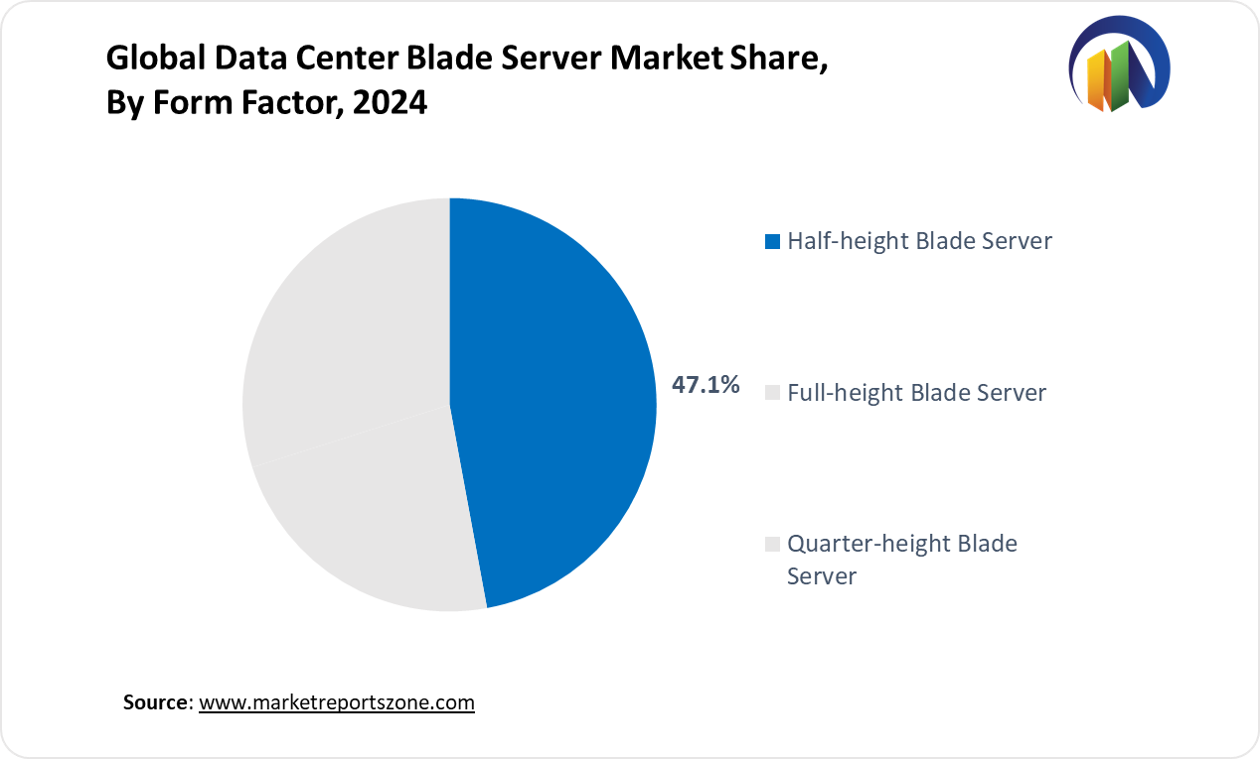

The data center blade server market is diverse, segmented by form factor, channel, application, and end-use. Half-height blade servers are widely used in enterprises for balanced performance and space efficiency. Full-height variants are preferred in AI-driven workloads, such as deep learning models used by pharmaceutical companies for drug discovery. Quarter-height servers find application in edge computing, enabling low-latency processing for autonomous vehicle networks. Direct sales dominate large-scale deployments, while resellers and system integrators cater to mid-sized businesses looking for customized solutions. In applications, virtualization and cloud computing drive demand as e-learning platforms scale their infrastructure.

High-performance computing supports scientific research, with meteorological organizations using blade servers for climate modeling. Storage and backup remain crucial, with media firms archiving vast digital content libraries. Web hosting providers depend on these servers for seamless online platform management. Database management sees adoption in retail for real-time inventory tracking. AI and machine learning workloads require optimized processing, with financial institutions using them for algorithmic trading. Among end-users, BFSI secures transactions, healthcare processes patient data, and energy firms optimize grid management. IT & telecom industries expand data infrastructure, while government & defense ensure secure data storage. Blade servers continue evolving, adapting to industry needs.

Regional Analysis:

The data center blade server market varies across regions, influenced by technological advancements, digital transformation, and industry demand. North America leads with rapid cloud adoption, with hyperscalers expanding data centers to support streaming platforms and e-commerce giants. Financial institutions rely on blade servers for fraud detection and high-frequency trading. In Europe, strict data regulations drive demand for private cloud solutions, with healthcare firms using blade servers for AI-driven diagnostics. Automotive manufacturers integrate them for smart factory automation and vehicle telematics. The Asia-Pacific region sees explosive growth due to rising internet penetration, with telecom providers deploying blade servers for 5G infrastructure.

E-commerce platforms scale operations with these servers to handle peak traffic during major sales events. In Latin America, growing digital banking fuels adoption, with fintech startups leveraging blade servers for secure transactions and AI-driven customer insights. Government initiatives push smart city development, requiring edge computing solutions. The Middle East & Africa region sees rising demand as oil and gas companies use blade servers for predictive maintenance and real-time data analytics. Expanding cloud service providers invest in data centers to support regional enterprises. As digital economies grow, blade servers remain crucial in enhancing efficiency, scalability, and innovation across industries.

Competitive Scenario:

The data center blade server market is witnessing significant advancements driven by major industry players. Dell Technologies has experienced a substantial increase in its AI server backlog, reaching $9 billion, with plans to ship $15 billion worth of AI servers this year. Cisco Systems has entered the AI server market by integrating Nvidia chips into its data center servers, aiming to compete with established providers. Super Micro Computer's stock has surged, positioning it as a top performer in the S&P 500, due to optimism surrounding potential lucrative AI server contracts. Hewlett Packard Enterprise (HPE) continues to innovate in cloud hardware designs through initiatives like Project Olympus, collaborating with the Open Compute Project to enhance data center efficiency.

IBM focuses on high-performance computing solutions, catering to the growing demands of AI and big data analytics. Lenovo is expanding its server portfolio to support diverse workloads, including edge computing and AI applications. Huawei and Inspur are strengthening their positions in the Asia-Pacific region, addressing the increasing need for scalable and efficient data center infrastructures. Oracle is enhancing its cloud services by integrating advanced blade server technologies to improve performance and reliability. These developments underscore the industry's commitment to meeting the evolving demands of modern data centers, emphasizing scalability, efficiency, and support for emerging technologies.

Data Center Blade Server Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 18.56 Billion |

| Revenue Forecast in 2033 | USD 42.81 Billion |

| Growth Rate | CAGR of 9.73% from 2025 to 2033 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2033 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Cisco Systems, Inc.; Dell Inc.; FUJITSU; Hewlett Packard Enterprise Development LP; Huawei; IBM; INSPUR Co., Ltd.; Lenovo; Oracle; Super Micro Computer, Inc.; Others |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Data Center Blade Server Market report is segmented as follows:

By Form Factor,

- Half-height Blade Server

- Full-height Blade Server

- Quarter-height Blade Server

By Channel,

- Direct

- Reseller

- Systems Integrator

- Others

By Application,

- Virtualization and Cloud Computing

- High-performance Computing (HPC)

- Storage and Backup

- Web Hosting

- Database Management

- AI and Machine Learning Workloads

By End-use,

- BFSI

- Healthcare

- Energy

- IT & Telecom

- Government & Defense

- Others

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East & Africa

Key Market Players,

- Cisco Systems, Inc.

- Dell Inc.

- FUJITSU

- Hewlett Packard Enterprise Development LP

- Huawei

- IBM

- INSPUR Co., Ltd.

- Lenovo

- Oracle

- Super Micro Computer, Inc.

- Others

Frequently Asked Questions

Research Objectives

- Proliferation and maturation of trade in the global Data Center Blade Server Market.

- The market share of the global Data Center Blade Server Market, supply and demand ratio, growth revenue, supply chain analysis, and business overview.

- Current and future market trends that are influencing the growth opportunities and growth rate of the global Data Center Blade Server Market.

- Feasibility study, new market insights, company profiles, investment return, market size of the global Data Center Blade Server Market.

Chapter 1 Data Center Blade Server Market Executive Summary

- 1.1 Data Center Blade Server Market Research Scope

- 1.2 Data Center Blade Server Market Estimates and Forecast (2021-2033)

- 1.2.1 Global Data Center Blade Server Market Value and Volume and Growth Rate (2021-2033)

- 1.2.2 Global Data Center Blade Server Market Price Trend (2021-2033)

- 1.3 Global Data Center Blade Server Market Value and Volume Comparison, by Form Factor (2021-2033)

- 1.3.1 Half-height Blade Server

- 1.3.2 Full-height Blade Server

- 1.3.3 Quarter-height Blade Server

- 1.4 Global Data Center Blade Server Market Value and Volume Comparison, by Channel (2021-2033)

- 1.4.1 Direct

- 1.4.2 Reseller

- 1.4.3 Systems Integrator

- 1.4.4 Others

- 1.5 Global Data Center Blade Server Market Value and Volume Comparison, by Application (2021-2033)

- 1.5.1 Virtualization and Cloud Computing

- 1.5.2 High-performance Computing (HPC)

- 1.5.3 Storage and Backup

- 1.5.4 Web Hosting

- 1.5.5 Database Management

- 1.5.6 AI and Machine Learning Workloads

- 1.6 Global Data Center Blade Server Market Value and Volume Comparison, by End-use (2021-2033)

- 1.6.1 BFSI

- 1.6.2 Healthcare

- 1.6.3 Energy

- 1.6.4 IT & Telecom

- 1.6.5 Government & Defense

- 1.6.6 Others

Chapter 2 Research Methodology

- 2.1 Introduction

- 2.2 Data Capture Sources

- 2.2.1 Primary Sources

- 2.2.2 Secondary Sources

- 2.3 Market Size Estimation

- 2.4 Market Forecast

- 2.5 Assumptions and Limitations

Chapter 3 Market Dynamics

- 3.1 Market Trends

- 3.2 Opportunities and Drivers

- 3.3 Challenges

- 3.4 Market Restraints

- 3.5 Porter's Five Forces Analysis

Chapter 4 Supply Chain Analysis and Marketing Channels

- 4.1 Data Center Blade Server Supply Chain Analysis

- 4.2 Marketing Channels

- 4.3 Data Center Blade Server Suppliers List

- 4.4 Data Center Blade Server Distributors List

- 4.5 Data Center Blade Server Customers

Chapter 5 COVID-19 & Russia–Ukraine War Impact Analysis

- 5.1 COVID-19 Impact Analysis on Data Center Blade Server Market

- 5.2 Russia-Ukraine War Impact Analysis on Data Center Blade Server Market

Chapter 6 Data Center Blade Server Market Estimate and Forecast by Region

- 6.1 Global Data Center Blade Server Market Value by Region: 2021 VS 2023 VS 2033

- 6.2 Global Data Center Blade Server Market Scenario by Region (2021-2023)

- 6.2.1 Global Data Center Blade Server Market Value and Volume Share by Region (2021-2023)

- 6.3 Global Data Center Blade Server Market Forecast by Region (2024-2033)

- 6.3.1 Global Data Center Blade Server Market Value and Volume Forecast by Region (2024-2033)

- 6.4 Geographic Market Analysis: Market Facts and Figures

- 6.4.1 North America Data Center Blade Server Market Estimates and Projections (2021-2033)

- 6.4.2 Europe Data Center Blade Server Market Estimates and Projections (2021-2033)

- 6.4.3 Asia Pacific Data Center Blade Server Market Estimates and Projections (2021-2033)

- 6.4.4 Latin America Data Center Blade Server Market Estimates and Projections (2021-2033)

- 6.4.5 Middle East & Africa Data Center Blade Server Market Estimates and Projections (2021-2033)

Chapter 7 Global Data Center Blade Server Competition Landscape by Players

- 7.1 Global Top Data Center Blade Server Players by Value (2021-2023)

- 7.2 Data Center Blade Server Headquarters and Sales Region by Company

- 7.3 Company Recent Developments, Mergers & Acquisitions, and Expansion Plans

Chapter 8 Global Data Center Blade Server Market, by Form Factor

- 8.1 Global Data Center Blade Server Market Value and Volume, by Form Factor (2021-2033)

- 8.1.1 Half-height Blade Server

- 8.1.2 Full-height Blade Server

- 8.1.3 Quarter-height Blade Server

Chapter 9 Global Data Center Blade Server Market, by Channel

- 9.1 Global Data Center Blade Server Market Value and Volume, by Channel (2021-2033)

- 9.1.1 Direct

- 9.1.2 Reseller

- 9.1.3 Systems Integrator

- 9.1.4 Others

Chapter 10 Global Data Center Blade Server Market, by Application

- 10.1 Global Data Center Blade Server Market Value and Volume, by Application (2021-2033)

- 10.1.1 Virtualization and Cloud Computing

- 10.1.2 High-performance Computing (HPC)

- 10.1.3 Storage and Backup

- 10.1.4 Web Hosting

- 10.1.5 Database Management

- 10.1.6 AI and Machine Learning Workloads

Chapter 11 Global Data Center Blade Server Market, by End-use

- 11.1 Global Data Center Blade Server Market Value and Volume, by End-use (2021-2033)

- 11.1.1 BFSI

- 11.1.2 Healthcare

- 11.1.3 Energy

- 11.1.4 IT & Telecom

- 11.1.5 Government & Defense

- 11.1.6 Others

Chapter 12 North America Data Center Blade Server Market

- 12.1 Overview

- 12.2 North America Data Center Blade Server Market Value and Volume, by Country (2021-2033)

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.2.3 Mexico

- 12.3 North America Data Center Blade Server Market Value and Volume, by Form Factor (2021-2033)

- 12.3.1 Half-height Blade Server

- 12.3.2 Full-height Blade Server

- 12.3.3 Quarter-height Blade Server

- 12.4 North America Data Center Blade Server Market Value and Volume, by Channel (2021-2033)

- 12.4.1 Direct

- 12.4.2 Reseller

- 12.4.3 Systems Integrator

- 12.4.4 Others

- 12.5 North America Data Center Blade Server Market Value and Volume, by Application (2021-2033)

- 12.5.1 Virtualization and Cloud Computing

- 12.5.2 High-performance Computing (HPC)

- 12.5.3 Storage and Backup

- 12.5.4 Web Hosting

- 12.5.5 Database Management

- 12.5.6 AI and Machine Learning Workloads

- 12.6 North America Data Center Blade Server Market Value and Volume, by End-use (2021-2033)

- 12.6.1 BFSI

- 12.6.2 Healthcare

- 12.6.3 Energy

- 12.6.4 IT & Telecom

- 12.6.5 Government & Defense

- 12.6.6 Others

Chapter 13 Europe Data Center Blade Server Market

- 13.1 Overview

- 13.2 Europe Data Center Blade Server Market Value and Volume, by Country (2021-2033)

- 13.2.1 UK

- 13.2.2 Germany

- 13.2.3 France

- 13.2.4 Spain

- 13.2.5 Italy

- 13.2.6 Russia

- 13.2.7 Rest of Europe

- 13.3 Europe Data Center Blade Server Market Value and Volume, by Form Factor (2021-2033)

- 13.3.1 Half-height Blade Server

- 13.3.2 Full-height Blade Server

- 13.3.3 Quarter-height Blade Server

- 13.4 Europe Data Center Blade Server Market Value and Volume, by Channel (2021-2033)

- 13.4.1 Direct

- 13.4.2 Reseller

- 13.4.3 Systems Integrator

- 13.4.4 Others

- 13.5 Europe Data Center Blade Server Market Value and Volume, by Application (2021-2033)

- 13.5.1 Virtualization and Cloud Computing

- 13.5.2 High-performance Computing (HPC)

- 13.5.3 Storage and Backup

- 13.5.4 Web Hosting

- 13.5.5 Database Management

- 13.5.6 AI and Machine Learning Workloads

- 13.6 Europe Data Center Blade Server Market Value and Volume, by End-use (2021-2033)

- 13.6.1 BFSI

- 13.6.2 Healthcare

- 13.6.3 Energy

- 13.6.4 IT & Telecom

- 13.6.5 Government & Defense

- 13.6.6 Others

Chapter 14 Asia Pacific Data Center Blade Server Market

- 14.1 Overview

- 14.2 Asia Pacific Data Center Blade Server Market Value and Volume, by Country (2021-2033)

- 14.2.1 China

- 14.2.2 Japan

- 14.2.3 India

- 14.2.4 South Korea

- 14.2.5 Australia

- 14.2.6 Southeast Asia

- 14.2.7 Rest of Asia Pacific

- 14.3 Asia Pacific Data Center Blade Server Market Value and Volume, by Form Factor (2021-2033)

- 14.3.1 Half-height Blade Server

- 14.3.2 Full-height Blade Server

- 14.3.3 Quarter-height Blade Server

- 14.4 Asia Pacific Data Center Blade Server Market Value and Volume, by Channel (2021-2033)

- 14.4.1 Direct

- 14.4.2 Reseller

- 14.4.3 Systems Integrator

- 14.4.4 Others

- 14.5 Asia Pacific Data Center Blade Server Market Value and Volume, by Application (2021-2033)

- 14.5.1 Virtualization and Cloud Computing

- 14.5.2 High-performance Computing (HPC)

- 14.5.3 Storage and Backup

- 14.5.4 Web Hosting

- 14.5.5 Database Management

- 14.5.6 AI and Machine Learning Workloads

- 14.6 Asia Pacific Data Center Blade Server Market Value and Volume, by End-use (2021-2033)

- 14.6.1 BFSI

- 14.6.2 Healthcare

- 14.6.3 Energy

- 14.6.4 IT & Telecom

- 14.6.5 Government & Defense

- 14.6.6 Others

Chapter 15 Latin America Data Center Blade Server Market

- 15.1 Overview

- 15.2 Latin America Data Center Blade Server Market Value and Volume, by Country (2021-2033)

- 15.2.1 Brazil

- 15.2.2 Argentina

- 15.2.3 Rest of Latin America

- 15.3 Latin America Data Center Blade Server Market Value and Volume, by Form Factor (2021-2033)

- 15.3.1 Half-height Blade Server

- 15.3.2 Full-height Blade Server

- 15.3.3 Quarter-height Blade Server

- 15.4 Latin America Data Center Blade Server Market Value and Volume, by Channel (2021-2033)

- 15.4.1 Direct

- 15.4.2 Reseller

- 15.4.3 Systems Integrator

- 15.4.4 Others

- 15.5 Latin America Data Center Blade Server Market Value and Volume, by Application (2021-2033)

- 15.5.1 Virtualization and Cloud Computing

- 15.5.2 High-performance Computing (HPC)

- 15.5.3 Storage and Backup

- 15.5.4 Web Hosting

- 15.5.5 Database Management

- 15.5.6 AI and Machine Learning Workloads

- 15.6 Latin America Data Center Blade Server Market Value and Volume, by End-use (2021-2033)

- 15.6.1 BFSI

- 15.6.2 Healthcare

- 15.6.3 Energy

- 15.6.4 IT & Telecom

- 15.6.5 Government & Defense

- 15.6.6 Others

Chapter 16 Middle East & Africa Data Center Blade Server Market

- 16.1 Overview

- 16.2 Middle East & Africa Data Center Blade Server Market Value and Volume, by Country (2021-2033)

- 16.2.1 Saudi Arabia

- 16.2.2 UAE

- 16.2.3 South Africa

- 16.2.4 Rest of Middle East & Africa

- 16.3 Middle East & Africa Data Center Blade Server Market Value and Volume, by Form Factor (2021-2033)

- 16.3.1 Half-height Blade Server

- 16.3.2 Full-height Blade Server

- 16.3.3 Quarter-height Blade Server

- 16.4 Middle East & Africa Data Center Blade Server Market Value and Volume, by Channel (2021-2033)

- 16.4.1 Direct

- 16.4.2 Reseller

- 16.4.3 Systems Integrator

- 16.4.4 Others

- 16.5 Middle East & Africa Data Center Blade Server Market Value and Volume, by Application (2021-2033)

- 16.5.1 Virtualization and Cloud Computing

- 16.5.2 High-performance Computing (HPC)

- 16.5.3 Storage and Backup

- 16.5.4 Web Hosting

- 16.5.5 Database Management

- 16.5.6 AI and Machine Learning Workloads

- 16.6 Middle East & Africa Data Center Blade Server Market Value and Volume, by End-use (2021-2033)

- 16.6.1 BFSI

- 16.6.2 Healthcare

- 16.6.3 Energy

- 16.6.4 IT & Telecom

- 16.6.5 Government & Defense

- 16.6.6 Others

Chapter 17 Company Profiles and Market Share Analysis: (Business Overview, Market Share Analysis, Products/Services Offered, Recent Developments)

- 17.1 Cisco Systems, Inc.

- 17.2 Dell Inc.

- 17.3 FUJITSU

- 17.4 Hewlett Packard Enterprise Development LP

- 17.5 Huawei

- 17.6 IBM

- 17.7 INSPUR Co., Ltd.

- 17.8 Lenovo

- 17.9 Oracle

- 17.10 Super Micro Computer, Inc.

- 17.11 Others

Report ID:

26

Published Date:

March 2025

Trusted by more than 10,500 organizations globally

Infaluble Methodology

Customization

Analyst Support

Targeted Market View