Global Health Wellness Foods Market, By Type (Fresh and Natural, Functional Foods and Beverages, Heat and Eat, On-the-Go Snacking, Ready to Cook (RTC), Ready to Eat (RTE)), By Nature, By Fat Content, By Category, By Free From Category, By Application, By Distribution Channel, and By Region - Trends and Forecast Analysis, 2021-2033

Publish Date: 2025-03-01 | Format: PDF | Category: Food and Beverage | Pages: 350

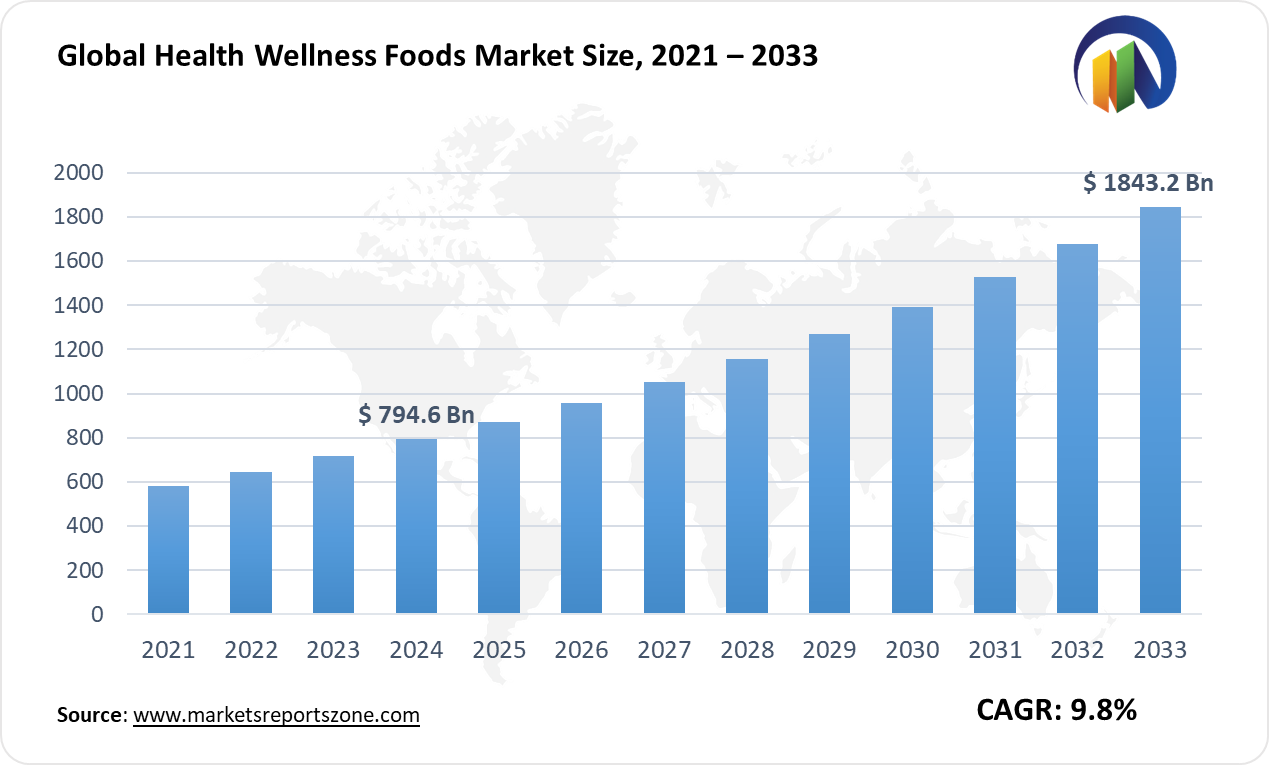

The Global Health Wellness Foods Market was valued at USD 794.6 Billion in 2024 and is projected to reach USD 1843.2 Billion by 2033 at a CAGR of around 9.8% between 2024 and 2033. The global health and wellness foods market is being driven by rising consumer awareness and lifestyle diseases. Demand for functional foods is increasing due to growing health consciousness. Products with natural ingredients and clean labels are being preferred. Regulatory support for nutritional food products is also strengthening market growth. However, high costs of organic and fortified foods are acting as a restraint. Affordability remains a challenge in price-sensitive markets. Despite this, opportunities are emerging through plant-based innovations and personalized nutrition.

Alternative proteins, such as pea and soy-based products, are being widely adopted. Companies like Nestlé and Danone are expanding plant-based dairy portfolios. AI-driven personalized nutrition is also gaining traction. Abbott and Herbalife are focusing on tailored health solutions. Immunity-boosting foods are being developed due to post-pandemic consumer demand. Probiotic-rich products from Yakult and Chobani are being widely accepted. Sustainable sourcing and eco-friendly packaging are being prioritized. PepsiCo and Mondelez are investing in regenerative agriculture. Consumer engagement through digital platforms is being enhanced. Online channels are being used for direct-to-consumer models. The market is continuously evolving with new product launches. Innovation and sustainability are shaping the future of health and wellness foods worldwide.

Driver: Rising Health Awareness Boosting Demand

Consumers are becoming more health-conscious, driving demand for nutritious foods. Awareness about lifestyle diseases like obesity and diabetes is increasing. People are actively choosing foods with functional benefits. Products fortified with vitamins, minerals, and antioxidants are gaining popularity. Heart-friendly oils, sugar-free snacks, and high-fiber cereals are being preferred. Brands are responding with innovative product formulations. Unilever has introduced cholesterol-lowering spreads for heart health. Kellogg’s is focusing on high-protein breakfast cereals. Coca-Cola is expanding its portfolio with low-calorie beverages. Functional beverages with adaptogens and collagen are also gaining traction. Startups are introducing turmeric-infused and plant-based wellness drinks.

Consumer interest in gut health is rising. Fermented foods like kimchi and kombucha are being widely accepted. E-commerce platforms are driving sales of wellness-focused products. Digital marketing is being used to educate consumers. Brands are highlighting product benefits on social media. Fitness influencers are promoting protein-packed and nutrient-rich foods. Restaurants are adapting to the trend with healthier menu options. Fast-food chains are launching plant-based and keto-friendly alternatives. The demand for clean-label and organic products is increasing. The health and wellness movement is reshaping the food industry. Companies are continuously innovating to meet evolving consumer preferences.

Key Insights:

- The global adoption rate of plant-based food products has crossed 15%, driven by increasing consumer demand for dairy and meat alternatives.

- Investments in alternative protein startups by major food companies have exceeded $5 billion in the past five years.

- Over 2 million metric tons of functional and fortified foods were sold globally last year, reflecting strong demand for health-oriented products.

- The penetration rate of organic food products in the packaged food industry has surpassed 10%, with steady growth in retail and e-commerce channels.

- Governments worldwide have allocated more than $2 billion in funding for food innovation, sustainability, and nutrition-focused R&D programs.

- The sales volume of probiotic-based dairy and beverages has reached nearly 800,000 tons, driven by rising interest in gut health.

- Investments in sustainable and eco-friendly packaging for health and wellness foods have crossed $1.5 billion, with brands focusing on recyclable and biodegradable materials.

- The share of sugar-free and reduced-sugar products in total snack sales has exceeded 20%, reflecting changing dietary preferences.

Segment Analysis:

The health and wellness foods market is evolving with diverse product offerings across multiple segments. Fresh and natural foods are gaining popularity as consumers prefer minimally processed options. Functional foods and beverages enriched with probiotics and vitamins support digestive health and immunity. Ready-to-cook and ready-to-eat meals provide convenience for busy lifestyles. On-the-go snacking is increasing, with brands like Nature Valley offering whole-grain snack bars. Non-GMO foods are favored by health-conscious consumers, while genetically modified options remain affordable alternatives. Low-fat, no-fat, and reduced-fat categories cater to weight-conscious buyers, with dairy brands expanding their fat-free yogurt range.

Organic products continue to grow, with farmers adopting sustainable practices. The demand for artificial color-free and gluten-free foods is rising, benefiting individuals with allergies. Sugar-free beverages are gaining traction, with brands introducing naturally sweetened sodas. Sports nutrition products, including protein powders and energy drinks, are essential for athletes. Clinical nutrition is expanding with meal replacements for medical needs. Supermarkets and hypermarkets remain dominant distribution channels, while online platforms provide easy access to specialized products. Pharmacies stock functional foods for targeted health benefits. As consumer awareness grows, companies continue to innovate with clean-label, nutritious offerings that align with evolving dietary preferences.

Regional Analysis:

The health and wellness foods market is expanding across all regions, driven by shifting dietary habits and rising health consciousness. In North America, plant-based protein products are in high demand, with brands like Beyond Meat offering meat alternatives for health-conscious consumers. Europe is witnessing strong growth in keto-friendly and high-protein snacks, with bakeries introducing low-carb bread and protein-enriched pastries. In Asia-Pacific, traditional ingredients are being blended into modern health foods, with companies launching matcha-infused energy bars and fermented foods like kimchi for gut health.

The Middle East and Africa are seeing a rise in dairy-free and sugar-free options, with brands launching almond milk and stevia-sweetened beverages to cater to dietary restrictions. Latin America is embracing superfoods, with local brands introducing chia seed-based drinks and quinoa-infused snacks. Supermarkets and hypermarkets dominate sales in developed regions, while e-commerce is growing rapidly in emerging markets. In Asia-Pacific, mobile apps and online platforms are making health foods more accessible. The Middle East is experiencing demand for halal-certified wellness products, ensuring compliance with dietary laws. As consumer preferences continue to evolve, brands are adapting with localized, nutrient-rich products that align with regional health trends and lifestyle choices.

Competition Landscape:

The global food and nutrition industry, driven by major players like Nestlé, Danone, PepsiCo, and General Mills, continues to evolve with a strong focus on health, sustainability, and innovation. Dairy giants such as Dairy Farmers of America and Glanbia are expanding into plant-based alternatives, while Yakult is leveraging probiotics for gut health awareness. Mondelez, Kraft Heinz, and Clif Bar are adapting to changing consumer preferences by reformulating snacks with cleaner labels and functional ingredients. Meanwhile, Abbott and GlaxoSmithKline are advancing in medical nutrition, targeting aging populations and performance nutrition.

Herbalife maintains its grip on personalized wellness trends, and ADM is pushing into alternative proteins and sustainable agriculture. Chobani’s expansion beyond yogurt into oat milk and coffee products reflects a broader industry shift toward diversification. PepsiCo and Danone are scaling up sustainability efforts, focusing on regenerative agriculture and carbon footprint reduction. Recent M&A activities, such as Mondelez acquiring Clif Bar, highlight ongoing consolidation strategies. Companies are also embracing digitalization, leveraging AI for supply chain efficiency and personalized nutrition solutions. Overall, the sector is balancing indulgence with health-conscious choices, sustainability with profitability, and legacy brands with innovative startups, shaping the future of global food and nutrition.

Health Wellness Foods Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 794.6 Billion |

| Revenue Forecast in 2033 | USD 1843.2 Billion |

| Growth Rate | CAGR of 9.8% from 2025 to 2033 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2033 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Nestlé S.A.; Danone S.A.; PepsiCo Inc.; General Mills Inc.; Kraft Heinz Company; Mondelez International Inc.; GlaxoSmithKline PLC; Abbott Laboratories; Herbalife Nutrition Ltd.; Archer Daniels Midland Company; Chobani Global Holdings LLC; Clif Bar & Company; Dairy Farmers of America Inc.; Glanbia PLC; Yakult Honsha Co., Ltd. |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Health Wellness Foods Market report is segmented as follows:

By Type,

- Fresh and Natural

- Functional Foods and Beverages

- Heat and Eat

- On-the-Go Snacking

- Ready to Cook (RTC)

- Ready to Eat (RTE)

By Nature,

- Genetically Modified Organism Food

- Non-Genetically Modified Organism Food

By Fat Content,

- Low Fat

- No Fat

- Reduced-Fat

By Category,

- Conventional

- Organic

By Free From Category,

- Artificial Color-Free

- Artificial Flavor-Free

- Gluten-Free

- Lactose-Free

- Nut-Free

- Soy-Free

- Sugar-free

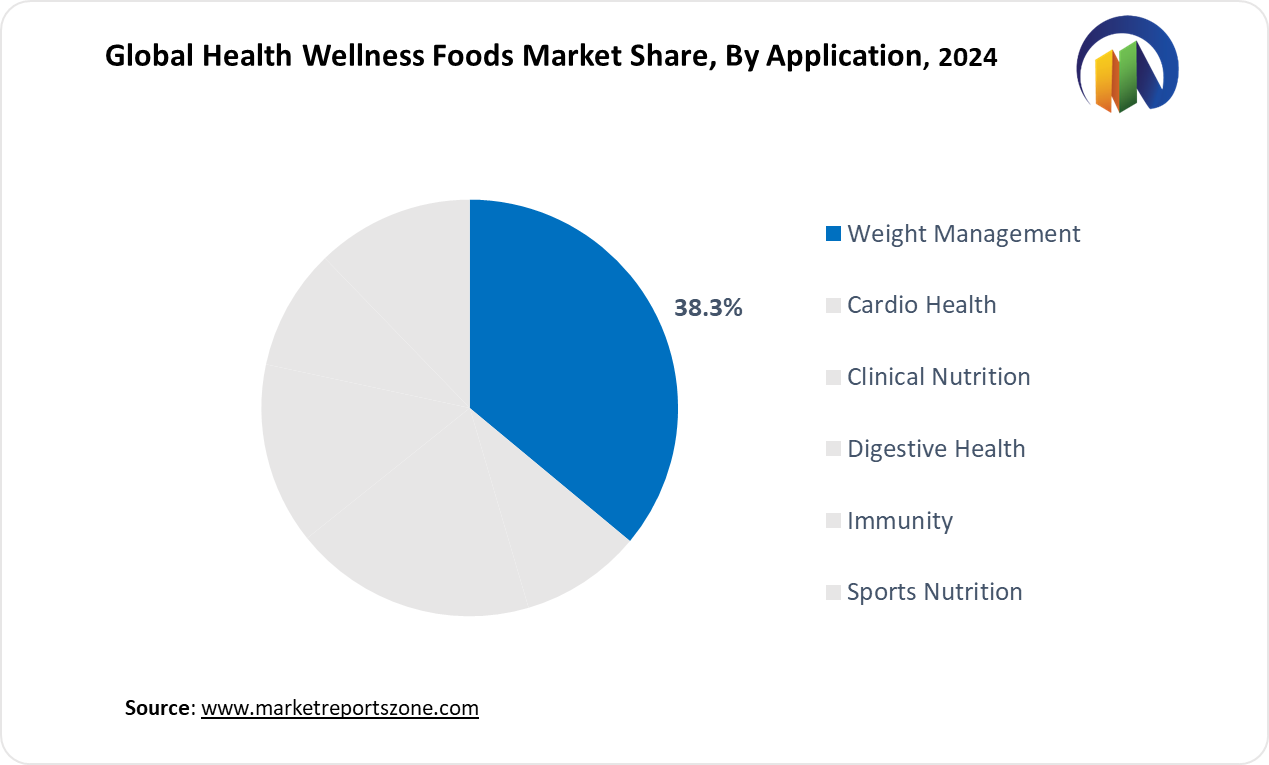

By Application,

- Cardio Health

- Clinical Nutrition

- Digestive Health

- Immunity

- Sports Nutrition

- Weight Management

By Distribution Channel,

- Convenience Stores

- Pharmacies and Drugstores

- Supermarkets and Hypermarket

- Online Mode

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East & Africa

Key Market Players,

- Nestle S.A.

- Danone S.A.

- PepsiCo Inc.

- General Mills Inc.

- Kraft Heinz Company

- Mondelez International Inc.

- GlaxoSmithKline PLC

- Abbott Laboratories

- Herbalife Nutrition Ltd.

- Archer Daniels Midland Company

- Chobani Global Holdings LLC

- Clif Bar & Company

- Dairy Farmers of America Inc.

- Glanbia PLC

- Yakult Honsha Co., Ltd.

Frequently Asked Questions

Research Objectives

- Proliferation and maturation of trade in the global Health Wellness Foods Market.

- The market share of the global Health Wellness Foods Market, supply and demand ratio, growth revenue, supply chain analysis, and business overview.

- Current and future market trends that are influencing the growth opportunities and growth rate of the global Health Wellness Foods Market.

- Feasibility study, new market insights, company profiles, investment return, market size of the global Health Wellness Foods Market.

Chapter 1 Health Wellness Foods Market Executive Summary

- 1.1 Health Wellness Foods Market Research Scope

- 1.2 Health Wellness Foods Market Estimates and Forecast (2021-2033)

- 1.2.1 Global Health Wellness Foods Market Value and Growth Rate (2021-2033)

- 1.2.2 Global Health Wellness Foods Market Price Trend (2021-2033)

- 1.3 Global Health Wellness Foods Market Value Comparison, by Type (2021-2033)

- 1.3.1 Fresh and Natural

- 1.3.2 Functional Foods and Beverages

- 1.3.3 Heat and Eat

- 1.3.4 On-the-Go Snacking

- 1.3.5 Ready to Cook (RTC)

- 1.3.6 Ready to Eat (RTE)

- 1.4 Global Health Wellness Foods Market Value Comparison, by Nature (2021-2033)

- 1.4.1 Genetically Modified Organism Food

- 1.4.2 Non-Genetically Modified Organism Food

- 1.5 Global Health Wellness Foods Market Value Comparison, by Fat Content (2021-2033)

- 1.5.1 Low Fat

- 1.5.2 No Fat

- 1.5.3 Reduced-Fat

- 1.6 Global Health Wellness Foods Market Value Comparison, by Category (2021-2033)

- 1.6.1 Conventional

- 1.6.2 Organic

- 1.7 Global Health Wellness Foods Market Value Comparison, by Free From Category (2021-2033)

- 1.7.1 Artificial Color-Free

- 1.7.2 Artificial Flavor-Free

- 1.7.3 Gluten-Free

- 1.7.4 Lactose-Free

- 1.7.5 Nut-Free

- 1.7.6 Soy-Free

- 1.7.7 Sugar-free

- 1.8 Global Health Wellness Foods Market Value Comparison, by Application (2021-2033)

- 1.8.1 Cardio Health

- 1.8.2 Clinical Nutrition

- 1.8.3 Digestive Health

- 1.8.4 Immunity

- 1.8.5 Sports Nutrition

- 1.8.6 Weight Management

- 1.9 Global Health Wellness Foods Market Value Comparison, by Distribution Channel (2021-2033)

- 1.9.1 Convenience Stores

- 1.9.2 Pharmacies and Drugstores

- 1.9.3 Supermarkets and Hypermarket

- 1.9.4 Online Mode

Chapter 2 Research Methodology

- 2.1 Introduction

- 2.2 Data Capture Sources

- 2.2.1 Primary Sources

- 2.2.2 Secondary Sources

- 2.3 Market Size Estimation

- 2.4 Market Forecast

- 2.5 Assumptions and Limitations

Chapter 3 Market Dynamics

- 3.1 Market Trends

- 3.2 Opportunities and Drivers

- 3.3 Challenges

- 3.4 Market Restraints

- 3.5 Porter's Five Forces Analysis

Chapter 4 Supply Chain Analysis and Marketing Channels

- 4.1 Health Wellness Foods Supply Chain Analysis

- 4.2 Marketing Channels

- 4.3 Health Wellness Foods Suppliers List

- 4.4 Health Wellness Foods Distributors List

- 4.5 Health Wellness Foods Customers

Chapter 5 COVID-19 & Russia–Ukraine War Impact Analysis

- 5.1 COVID-19 Impact Analysis on Health Wellness Foods Market

- 5.2 Russia-Ukraine War Impact Analysis on Health Wellness Foods Market

Chapter 6 Health Wellness Foods Market Estimate and Forecast by Region

- 6.1 Global Health Wellness Foods Market Value by Region: 2021 VS 2023 VS 2033

- 6.2 Global Health Wellness Foods Market Scenario by Region (2021-2023)

- 6.2.1 Global Health Wellness Foods Market Value Share by Region (2021-2023)

- 6.3 Global Health Wellness Foods Market Forecast by Region (2024-2033)

- 6.3.1 Global Health Wellness Foods Market Value Forecast by Region (2024-2033)

- 6.4 Geographic Market Analysis: Market Facts and Figures

- 6.4.1 North America Health Wellness Foods Market Estimates and Projections (2021-2033)

- 6.4.2 Europe Health Wellness Foods Market Estimates and Projections (2021-2033)

- 6.4.3 Asia Pacific Health Wellness Foods Market Estimates and Projections (2021-2033)

- 6.4.4 Latin America Health Wellness Foods Market Estimates and Projections (2021-2033)

- 6.4.5 Middle East & Africa Health Wellness Foods Market Estimates and Projections (2021-2033)

Chapter 7 Global Health Wellness Foods Competition Landscape by Players

- 7.1 Global Top Health Wellness Foods Players by Value (2021-2023)

- 7.2 Health Wellness Foods Headquarters and Sales Region by Company

- 7.3 Company Recent Developments, Mergers & Acquisitions, and Expansion Plans

Chapter 8 Global Health Wellness Foods Market, by Type

- 8.1 Global Health Wellness Foods Market Value, by Type (2021-2033)

- 8.1.1 Fresh and Natural

- 8.1.2 Functional Foods and Beverages

- 8.1.3 Heat and Eat

- 8.1.4 On-the-Go Snacking

- 8.1.5 Ready to Cook (RTC)

- 8.1.6 Ready to Eat (RTE)

Chapter 9 Global Health Wellness Foods Market, by Nature

- 9.1 Global Health Wellness Foods Market Value, by Nature (2021-2033)

- 9.1.1 Genetically Modified Organism Food

- 9.1.2 Non-Genetically Modified Organism Food

Chapter 10 Global Health Wellness Foods Market, by Fat Content

- 10.1 Global Health Wellness Foods Market Value, by Fat Content (2021-2033)

- 10.1.1 Low Fat

- 10.1.2 No Fat

- 10.1.3 Reduced-Fat

Chapter 11 Global Health Wellness Foods Market, by Category

- 11.1 Global Health Wellness Foods Market Value, by Category (2021-2033)

- 11.1.1 Conventional

- 11.1.2 Organic

Chapter 12 Global Health Wellness Foods Market, by Free From Category

- 12.1 Global Health Wellness Foods Market Value, by Free From Category (2021-2033)

- 12.1.1 Artificial Color-Free

- 12.1.2 Artificial Flavor-Free

- 12.1.3 Gluten-Free

- 12.1.4 Lactose-Free

- 12.1.5 Nut-Free

- 12.1.6 Soy-Free

- 12.1.7 Sugar-free

Chapter 13 Global Health Wellness Foods Market, by Application

- 13.1 Global Health Wellness Foods Market Value, by Application (2021-2033)

- 13.1.1 Cardio Health

- 13.1.2 Clinical Nutrition

- 13.1.3 Digestive Health

- 13.1.4 Immunity

- 13.1.5 Sports Nutrition

- 13.1.6 Weight Management

Chapter 14 Global Health Wellness Foods Market, by Distribution Channel

- 14.1 Global Health Wellness Foods Market Value, by Distribution Channel (2021-2033)

- 14.1.1 Convenience Stores

- 14.1.2 Pharmacies and Drugstores

- 14.1.3 Supermarkets and Hypermarket

- 14.1.4 Online Mode

Chapter 15 North America Health Wellness Foods Market

- 15.1 Overview

- 15.2 North America Health Wellness Foods Market Value, by Country (2021-2033)

- 15.2.1 U.S.

- 15.2.2 Canada

- 15.2.3 Mexico

- 15.3 North America Health Wellness Foods Market Value, by Type (2021-2033)

- 15.3.1 Fresh and Natural

- 15.3.2 Functional Foods and Beverages

- 15.3.3 Heat and Eat

- 15.3.4 On-the-Go Snacking

- 15.3.5 Ready to Cook (RTC)

- 15.3.6 Ready to Eat (RTE)

- 15.4 North America Health Wellness Foods Market Value, by Nature (2021-2033)

- 15.4.1 Genetically Modified Organism Food

- 15.4.2 Non-Genetically Modified Organism Food

- 15.5 North America Health Wellness Foods Market Value, by Fat Content (2021-2033)

- 15.5.1 Low Fat

- 15.5.2 No Fat

- 15.5.3 Reduced-Fat

- 15.6 North America Health Wellness Foods Market Value, by Category (2021-2033)

- 15.6.1 Conventional

- 15.6.2 Organic

- 15.7 North America Health Wellness Foods Market Value, by Free From Category (2021-2033)

- 15.7.1 Artificial Color-Free

- 15.7.2 Artificial Flavor-Free

- 15.7.3 Gluten-Free

- 15.7.4 Lactose-Free

- 15.7.5 Nut-Free

- 15.7.6 Soy-Free

- 15.7.7 Sugar-free

- 15.8 North America Health Wellness Foods Market Value, by Application (2021-2033)

- 15.8.1 Cardio Health

- 15.8.2 Clinical Nutrition

- 15.8.3 Digestive Health

- 15.8.4 Immunity

- 15.8.5 Sports Nutrition

- 15.8.6 Weight Management

- 15.9 North America Health Wellness Foods Market Value, by Distribution Channel (2021-2033)

- 15.9.1 Convenience Stores

- 15.9.2 Pharmacies and Drugstores

- 15.9.3 Supermarkets and Hypermarket

- 15.9.4 Online Mode

Chapter 16 Europe Health Wellness Foods Market

- 16.1 Overview

- 16.2 Europe Health Wellness Foods Market Value, by Country (2021-2033)

- 16.2.1 UK

- 16.2.2 Germany

- 16.2.3 France

- 16.2.4 Spain

- 16.2.5 Italy

- 16.2.6 Russia

- 16.2.7 Rest of Europe

- 16.3 Europe Health Wellness Foods Market Value, by Type (2021-2033)

- 16.3.1 Fresh and Natural

- 16.3.2 Functional Foods and Beverages

- 16.3.3 Heat and Eat

- 16.3.4 On-the-Go Snacking

- 16.3.5 Ready to Cook (RTC)

- 16.3.6 Ready to Eat (RTE)

- 16.4 Europe Health Wellness Foods Market Value, by Nature (2021-2033)

- 16.4.1 Genetically Modified Organism Food

- 16.4.2 Non-Genetically Modified Organism Food

- 16.5 Europe Health Wellness Foods Market Value, by Fat Content (2021-2033)

- 16.5.1 Low Fat

- 16.5.2 No Fat

- 16.5.3 Reduced-Fat

- 16.6 Europe Health Wellness Foods Market Value, by Category (2021-2033)

- 16.6.1 Conventional

- 16.6.2 Organic

- 16.7 Europe Health Wellness Foods Market Value, by Free From Category (2021-2033)

- 16.7.1 Artificial Color-Free

- 16.7.2 Artificial Flavor-Free

- 16.7.3 Gluten-Free

- 16.7.4 Lactose-Free

- 16.7.5 Nut-Free

- 16.7.6 Soy-Free

- 16.7.7 Sugar-free

- 16.8 Europe Health Wellness Foods Market Value, by Application (2021-2033)

- 16.8.1 Cardio Health

- 16.8.2 Clinical Nutrition

- 16.8.3 Digestive Health

- 16.8.4 Immunity

- 16.8.5 Sports Nutrition

- 16.8.6 Weight Management

- 16.9 Europe Health Wellness Foods Market Value, by Distribution Channel (2021-2033)

- 16.9.1 Convenience Stores

- 16.9.2 Pharmacies and Drugstores

- 16.9.3 Supermarkets and Hypermarket

- 16.9.4 Online Mode

Chapter 17 Asia Pacific Health Wellness Foods Market

- 17.1 Overview

- 17.2 Asia Pacific Health Wellness Foods Market Value, by Country (2021-2033)

- 17.2.1 China

- 17.2.2 Japan

- 17.2.3 India

- 17.2.4 South Korea

- 17.2.5 Australia

- 17.2.6 Southeast Asia

- 17.2.7 Rest of Asia Pacific

- 17.3 Asia Pacific Health Wellness Foods Market Value, by Type (2021-2033)

- 17.3.1 Fresh and Natural

- 17.3.2 Functional Foods and Beverages

- 17.3.3 Heat and Eat

- 17.3.4 On-the-Go Snacking

- 17.3.5 Ready to Cook (RTC)

- 17.3.6 Ready to Eat (RTE)

- 17.4 Asia Pacific Health Wellness Foods Market Value, by Nature (2021-2033)

- 17.4.1 Genetically Modified Organism Food

- 17.4.2 Non-Genetically Modified Organism Food

- 17.5 Asia Pacific Health Wellness Foods Market Value, by Fat Content (2021-2033)

- 17.5.1 Low Fat

- 17.5.2 No Fat

- 17.5.3 Reduced-Fat

- 17.6 Asia Pacific Health Wellness Foods Market Value, by Category (2021-2033)

- 17.6.1 Conventional

- 17.6.2 Organic

- 17.7 Asia Pacific Health Wellness Foods Market Value, by Free From Category (2021-2033)

- 17.7.1 Artificial Color-Free

- 17.7.2 Artificial Flavor-Free

- 17.7.3 Gluten-Free

- 17.7.4 Lactose-Free

- 17.7.5 Nut-Free

- 17.7.6 Soy-Free

- 17.7.7 Sugar-free

- 17.8 Asia Pacific Health Wellness Foods Market Value, by Application (2021-2033)

- 17.8.1 Cardio Health

- 17.8.2 Clinical Nutrition

- 17.8.3 Digestive Health

- 17.8.4 Immunity

- 17.8.5 Sports Nutrition

- 17.8.6 Weight Management

- 17.9 Asia Pacific Health Wellness Foods Market Value, by Distribution Channel (2021-2033)

- 17.9.1 Convenience Stores

- 17.9.2 Pharmacies and Drugstores

- 17.9.3 Supermarkets and Hypermarket

- 17.9.4 Online Mode

Chapter 18 Latin America Health Wellness Foods Market

- 18.1 Overview

- 18.2 Latin America Health Wellness Foods Market Value, by Country (2021-2033)

- 18.2.1 Brazil

- 18.2.2 Argentina

- 18.2.3 Rest of Latin America

- 18.3 Latin America Health Wellness Foods Market Value, by Type (2021-2033)

- 18.3.1 Fresh and Natural

- 18.3.2 Functional Foods and Beverages

- 18.3.3 Heat and Eat

- 18.3.4 On-the-Go Snacking

- 18.3.5 Ready to Cook (RTC)

- 18.3.6 Ready to Eat (RTE)

- 18.4 Latin America Health Wellness Foods Market Value, by Nature (2021-2033)

- 18.4.1 Genetically Modified Organism Food

- 18.4.2 Non-Genetically Modified Organism Food

- 18.5 Latin America Health Wellness Foods Market Value, by Fat Content (2021-2033)

- 18.5.1 Low Fat

- 18.5.2 No Fat

- 18.5.3 Reduced-Fat

- 18.6 Latin America Health Wellness Foods Market Value, by Category (2021-2033)

- 18.6.1 Conventional

- 18.6.2 Organic

- 18.7 Latin America Health Wellness Foods Market Value, by Free From Category (2021-2033)

- 18.7.1 Artificial Color-Free

- 18.7.2 Artificial Flavor-Free

- 18.7.3 Gluten-Free

- 18.7.4 Lactose-Free

- 18.7.5 Nut-Free

- 18.7.6 Soy-Free

- 18.7.7 Sugar-free

- 18.8 Latin America Health Wellness Foods Market Value, by Application (2021-2033)

- 18.8.1 Cardio Health

- 18.8.2 Clinical Nutrition

- 18.8.3 Digestive Health

- 18.8.4 Immunity

- 18.8.5 Sports Nutrition

- 18.8.6 Weight Management

- 18.9 Latin America Health Wellness Foods Market Value, by Distribution Channel (2021-2033)

- 18.9.1 Convenience Stores

- 18.9.2 Pharmacies and Drugstores

- 18.9.3 Supermarkets and Hypermarket

- 18.9.4 Online Mode

Chapter 19 Middle East & Africa Health Wellness Foods Market

- 19.1 Overview

- 19.2 Middle East & Africa Health Wellness Foods Market Value, by Country (2021-2033)

- 19.2.1 Saudi Arabia

- 19.2.2 UAE

- 19.2.3 South Africa

- 19.2.4 Rest of Middle East & Africa

- 19.3 Middle East & Africa Health Wellness Foods Market Value, by Type (2021-2033)

- 19.3.1 Fresh and Natural

- 19.3.2 Functional Foods and Beverages

- 19.3.3 Heat and Eat

- 19.3.4 On-the-Go Snacking

- 19.3.5 Ready to Cook (RTC)

- 19.3.6 Ready to Eat (RTE)

- 19.4 Middle East & Africa Health Wellness Foods Market Value, by Nature (2021-2033)

- 19.4.1 Genetically Modified Organism Food

- 19.4.2 Non-Genetically Modified Organism Food

- 19.5 Middle East & Africa Health Wellness Foods Market Value, by Fat Content (2021-2033)

- 19.5.1 Low Fat

- 19.5.2 No Fat

- 19.5.3 Reduced-Fat

- 19.6 Middle East & Africa Health Wellness Foods Market Value, by Category (2021-2033)

- 19.6.1 Conventional

- 19.6.2 Organic

- 19.7 Middle East & Africa Health Wellness Foods Market Value, by Free From Category (2021-2033)

- 19.7.1 Artificial Color-Free

- 19.7.2 Artificial Flavor-Free

- 19.7.3 Gluten-Free

- 19.7.4 Lactose-Free

- 19.7.5 Nut-Free

- 19.7.6 Soy-Free

- 19.7.7 Sugar-free

- 19.8 Middle East & Africa Health Wellness Foods Market Value, by Application (2021-2033)

- 19.8.1 Cardio Health

- 19.8.2 Clinical Nutrition

- 19.8.3 Digestive Health

- 19.8.4 Immunity

- 19.8.5 Sports Nutrition

- 19.8.6 Weight Management

- 19.9 Middle East & Africa Health Wellness Foods Market Value, by Distribution Channel (2021-2033)

- 19.9.1 Convenience Stores

- 19.9.2 Pharmacies and Drugstores

- 19.9.3 Supermarkets and Hypermarket

- 19.9.4 Online Mode

Chapter 20 Company Profiles and Market Share Analysis: (Business Overview, Market Share Analysis, Products/Services Offered, Recent Developments)

- 20.1 Nestlé S.A.

- 20.2 Danone S.A.

- 20.3 PepsiCo Inc.

- 20.4 General Mills Inc.

- 20.5 Kraft Heinz Company

- 20.6 Mondelez International Inc.

- 20.7 GlaxoSmithKline PLC

- 20.8 Abbott Laboratories

- 20.9 Herbalife Nutrition Ltd.

- 20.10 Archer Daniels Midland Company

- 20.11 Chobani Global Holdings LLC

- 20.12 Clif Bar & Company

- 20.13 Dairy Farmers of America Inc.

- 20.14 Glanbia PLC

- 20.15 Yakult Honsha Co., Ltd.

Report ID:

12

Published Date:

March 2025

Trusted by more than 10,500 organizations globally

Infaluble Methodology

Customization

Analyst Support

Targeted Market View