Global Isoproterenol Market - Size and Forecast Analysis, 2021-2035

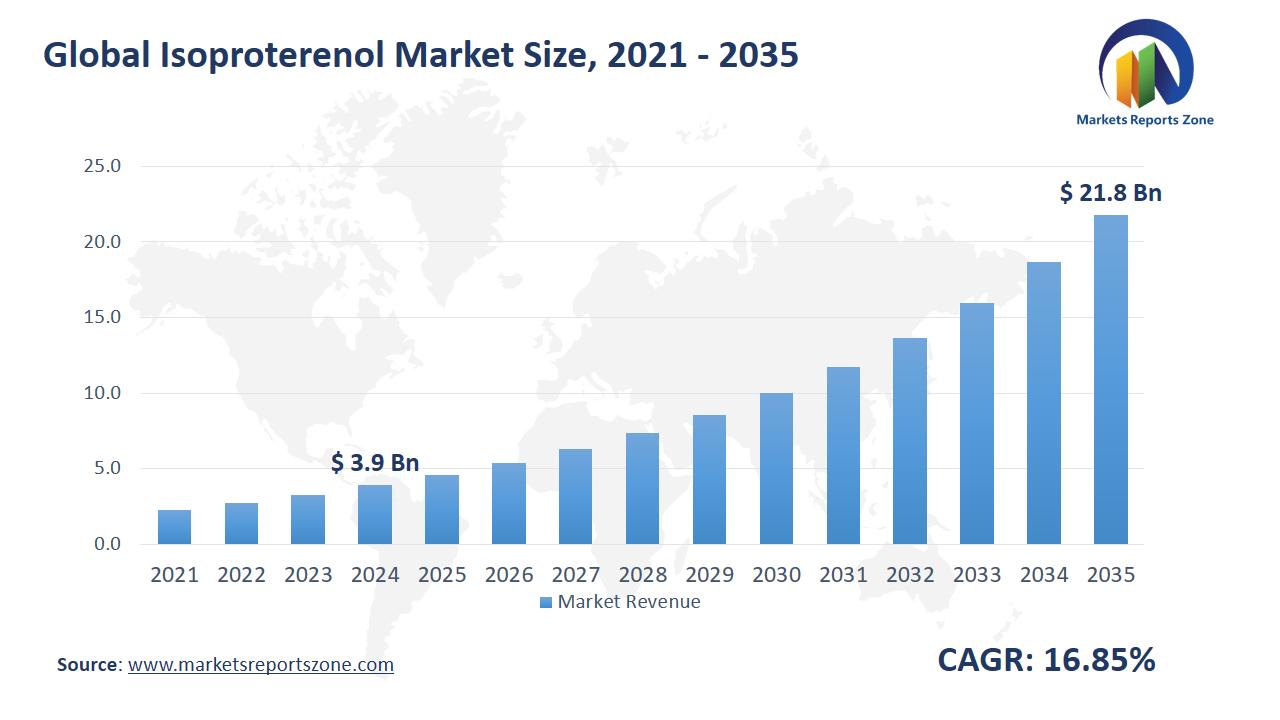

Global Isoproterenol Market Size is expected to reach USD 21.81 Billion by 2035 from USD 3.93 Billion in 2024, with a CAGR of around 16.85% between 2024 and 2035. The global isoproterenol market is experiencing growth driven by two main factors. Firstly, the increasing prevalence of cardiovascular diseases, particularly bradycardia and heart block, has led to a higher demand for isoproterenol as an effective treatment option. For example, in aging populations, where such conditions are more common, isoproterenol has been utilized to manage heart rhythm disorders. Secondly, advancements in drug delivery systems have enhanced the administration of isoproterenol, improving patient compliance and therapeutic outcomes. Innovations such as inhalers and nebulizers have facilitated easier use, especially for patients with respiratory conditions. However, the market faces restraints due to stringent regulatory requirements, which can delay the approval and availability of isoproterenol products. Despite this, opportunities exist in emerging markets where improving healthcare infrastructure is expanding access to cardiovascular treatments. Additionally, ongoing research into novel formulations and therapeutic applications of isoproterenol presents potential for market expansion. For instance, exploring its use in combination therapies could open new avenues for treating complex cardiovascular conditions.

Driver: Rising Heart Disorders Boost Demand

The increasing burden of cardiovascular diseases has strongly driven the demand for isoproterenol in recent years. As a life-saving drug for managing arrhythmias, especially bradycardia and atrioventricular block, its role has become more vital in both emergency and long-term settings. In urban hospitals, isoproterenol has been administered intravenously to stabilize patients experiencing sudden heart rate drops due to conduction issues. In many cases, elderly individuals, particularly those in assisted living facilities, have been treated with isoproterenol before being fitted with pacemakers. The drug’s ability to temporarily increase heart rate and improve cardiac output has made it indispensable in these situations. Even in rural clinics with limited access to advanced interventions, isoproterenol has been stocked as a critical care option, often used in ambulances during transport. Pediatric cardiology units have also begun using the medication to manage congenital conduction defects while preparing for surgical intervention. This growing usage reflects how healthcare providers are relying on isoproterenol not just for traditional cardiac emergencies but also for broader therapeutic applications. As the global incidence of heart diseases continues to rise, the demand for reliable and effective pharmacologic solutions like isoproterenol is only expected to grow further.

Key Insights:

The adoption rate of Isoproterenol in emergency medical settings for treating bradycardia and heart block is approximately 30%, driven by its effectiveness as a cardiac stimulant.

In 2023, pharmaceutical companies invested around $50 million in research and development for improving the formulation and delivery systems of Isoproterenol.

The total number of Isoproterenol units sold globally reached approximately 10 million units in 2024, reflecting its widespread use in both respiratory and cardiovascular treatments.

The penetration rate of Isoproterenol in respiratory care, particularly for asthma and COPD, is estimated to be about 40%, highlighting its role as a bronchodilator.

Major healthcare organizations have collectively invested over $100 million in expanding access to essential medications like Isoproterenol in emerging markets.

The average annual growth rate for Isoproterenol adoption has been reported at around 5% since 2022, driven by advancements in medical technology and increasing healthcare awareness.

By the end of 2024, the cumulative number of patients treated with Isoproterenol worldwide is expected to exceed 50 million, reflecting its critical role in managing acute and chronic conditions.

The use of Isoproterenol in combination therapies, such as with ACE inhibitors or beta-blockers, accounts for approximately 25% of its total applications, highlighting its versatility in complex cardiovascular treatments.

Segment Analysis:

The Isoproterenol market has been shaped by its delivery forms and focused application in heart block management. Aerosol forms have been commonly used in respiratory distress cases, especially for patients with overlapping pulmonary and cardiac conditions. In emergency rooms, aerosol isoproterenol has been administered to ease breathing and stimulate heart activity in patients with both asthma and bradycardia symptoms. Injectable forms remain the backbone of acute care. In cardiac care units, injectable isoproterenol has been used to stabilize patients with complete heart block while awaiting pacemaker insertion. Its rapid onset has been particularly useful in trauma centers and ambulances, where time-sensitive intervention is critical. Solution-based forms have been integrated into infusion systems for long-duration treatments. For instance, in intensive care units, patients with recurring conduction issues have been placed on continuous isoproterenol drips to maintain stable heart rates overnight. The core application across all types remains heart block, where patients experience dangerously low heart rates due to signal disruption between the atria and ventricles. In rural clinics, where advanced cardiac equipment is limited, these various forms of isoproterenol offer practical treatment routes. The diversity in administration methods has enabled its use across age groups, hospital settings, and levels of healthcare infrastructure.

Regional Analysis:

In North America, the Isoproterenol market has been driven by well-established emergency care infrastructure. In Canadian paramedic units, isoproterenol injections have been used during transport for patients with acute heart block. In Europe, especially in Germany and France, the preference for injectable forms has grown in cardiac rehab centers, where patients are monitored post-surgery and need temporary heart rate support. In Asia-Pacific, increased investment in rural healthcare has boosted the use of aerosol and solution forms. For example, in rural India, isoproterenol aerosols have been included in mobile medical kits used in community outreach vans to manage bradycardia episodes. In Latin America, especially Brazil, the drug has been adopted in government-funded health units. Local hospitals in Rio have been using it to bridge patients until pacemakers can be installed. Meanwhile, the Middle East and Africa have focused on improving access to essential cardiovascular drugs in underserved areas. Clinics in parts of South Africa have started using solution-based isoproterenol for nighttime cardiac monitoring in stroke rehabilitation wards. Across all regions, varying access levels and infrastructure have defined the way isoproterenol is administered, but its role in treating life-threatening heart rate conditions continues to be crucial in both urban and remote healthcare environments.

Competitive Scenario:

The Isoproterenol market has seen significant developments among key pharmaceutical companies focusing on expanding their cardiovascular portfolios. Sanofi Aventis US has continued to strengthen its position in the cardiovascular sector, although specific recent developments regarding Isoproterenol are not prominently reported. Hospira, known for its injectable drug offerings, has maintained its role in supplying critical care medications, including Isoproterenol, to healthcare facilities. Nexus Pharmaceuticals achieved a milestone with the FDA approval of its Isoproterenol Hydrochloride Injection, providing a generic equivalent to existing treatments. This approval has enabled Nexus to offer a cost-effective alternative for managing conditions like heart block and cardiac arrest. These collective efforts by pharmaceutical companies have enhanced the availability and affordability of Isoproterenol, contributing to improved patient care in cardiac emergencies.

Isoproterenol Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 3.93 Billion |

| Revenue Forecast in 2035 | USD 21.81 Billion |

| Growth Rate | CAGR of 16.85% from 2025 to 2035 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2035 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | SANOFI AVENTIS US; HOSPIRA; SANOFI AVENTIS US; NEXUS PHARMS |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Isoproterenol Market report is segmented as follows:

By Type,

- Aerosol

- Injectable

- Solution

By Application,

- Heart Block

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

Key Market Players,

- SANOFI AVENTIS US

- HOSPIRA

- SANOFI AVENTIS US

- NEXUS PHARMS

Frequently Asked Questions

How big is the Isoproterenol market?

Global Isoproterenol Market Size was valued at USD 3.93 Billion in 2024 and is projected to reach at USD 21.81 Billion in 2035.

What is the Isoproterenol market growth?

Global Isoproterenol Market is expected to grow at a CAGR of around 16.85% during the forecasted year.

Which region has the largest market share in Isoproterenol market?

North America, Asia Pacific and Europe are major regions in the global Isoproterenol Market.

Who are the key players in Isoproterenol market?

Key players analyzed in the global Isoproterenol Market are SANOFI AVENTIS US; HOSPIRA; SANOFI AVENTIS US; NEXUS PHARMS and so on.