Global Medical Vacuum Systems Market - Size and Forecast Analysis, 2021-2035

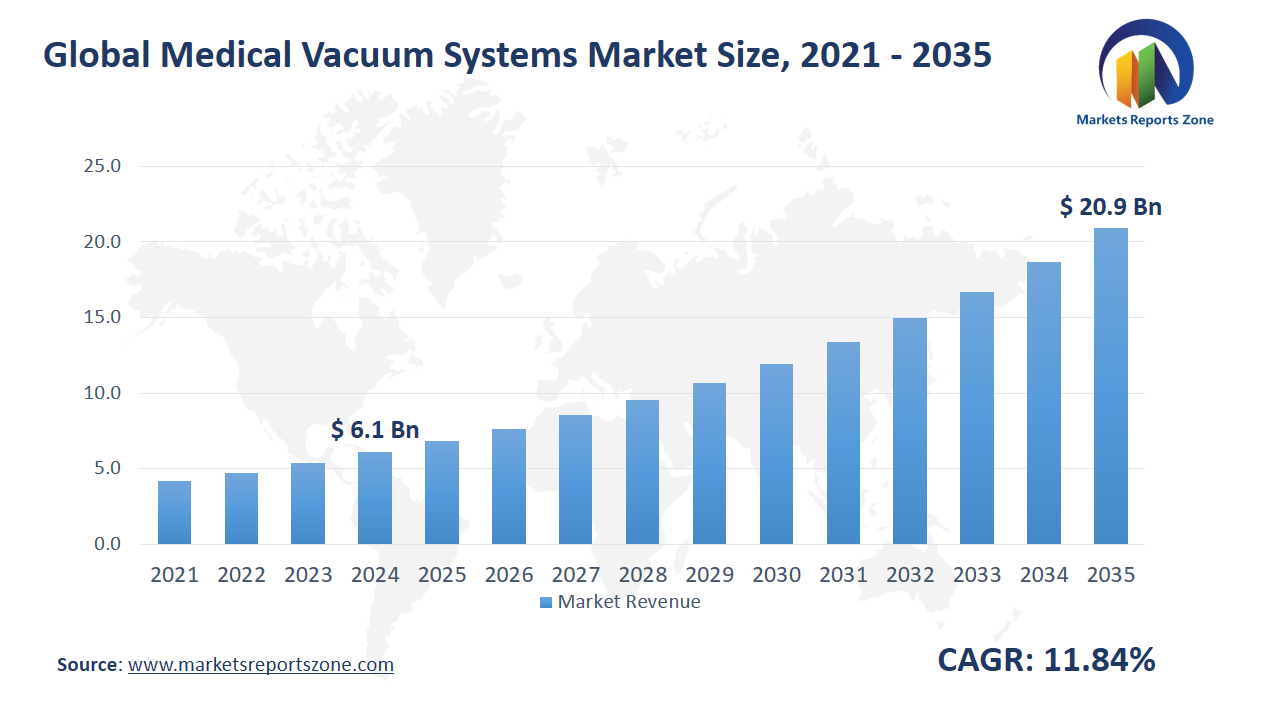

Global Medical Vacuum Systems Market Size is expected to reach USD 20.91 Billion by 2035 from USD 6.1 Billion in 2024, with a CAGR of around 11.84% between 2024 and 2035. The global medical vacuum systems market is primarily driven by the increasing demand for advanced healthcare infrastructure and the growing need for infection control in hospitals and clinics. The rise in complex surgeries and critical care procedures, such as in operating rooms and intensive care units, necessitates the use of efficient vacuum systems to maintain a sterile environment. For example, vacuum systems are used to remove fluids and gases during surgeries, ensuring patient safety and minimizing infection risks. Additionally, the shift towards patient-centric care and enhanced hospital management has spurred investments in modern vacuum systems. However, the high installation and maintenance costs of these systems pose a significant restraint, limiting their adoption in smaller healthcare facilities. Despite this challenge, there are opportunities for market growth. The increasing number of outpatient procedures, such as dental treatments, provides a chance for vacuum systems to be integrated into various clinics. Moreover, the expanding healthcare infrastructure in emerging markets presents a significant opportunity for the market. Countries in Asia and Latin America are witnessing rapid development in medical facilities, creating demand for advanced medical equipment, including vacuum systems, which can enhance operational efficiency and improve patient outcomes in these regions.

Driver: Growing Need for Infection Control

Infection control has become a critical driver for the medical vacuum systems market. Hospitals and healthcare facilities are prioritizing infection prevention due to the rise in hospital-acquired infections (HAIs) and antimicrobial resistance. Effective vacuum systems help maintain a sterile environment, which is crucial for patient safety, particularly during surgeries and other invasive procedures. For example, in dental clinics, vacuum systems are used to remove saliva, blood, and other fluids during procedures, preventing contamination and ensuring a hygienic space. In operating rooms, medical vacuum systems are employed to manage smoke and fluids that could potentially lead to infections or complications if not properly handled. Additionally, intensive care units (ICUs) rely heavily on vacuum systems to support ventilators, which assist in the breathing of critically ill patients. These systems also help in the efficient drainage of bodily fluids from surgical wounds, reducing the risk of infection and promoting faster recovery. In modern hospitals, vacuum systems are essential in ensuring high standards of hygiene and patient care. The growing emphasis on infection control across the healthcare sector has significantly increased the demand for these systems, ensuring their continued role in safeguarding patient health during medical treatments.

Key Insights:

The adoption rate of medical robotics in surgical procedures has increased significantly, with robotic-assisted surgeries rising from 0% to 22% in the U.S. between 2012 and 2022.

In 2023, major healthcare companies invested around $1 billion in research and development for advanced medical robotics technologies.

The total number of robotic-assisted surgeries performed globally reached approximately 1.24 million in 2020, reflecting a growing trend towards minimally invasive procedures.

The penetration rate of medical robotics in general surgery applications is estimated to be about 23%, with a projected increase to 87% by 2030.

The average annual growth rate for the adoption of medical robotics has been reported at around 15%, driven by advancements in technology and increasing demand for precision surgeries.

By the end of 2024, the cumulative number of medical facilities equipped with robotic surgery systems worldwide is expected to exceed 5,000.

The use of medical robotics in cardiovascular surgeries accounts for approximately 10% of its total applications, highlighting its expanding role in treating chronic conditions.

Innovations in autonomous surgical robots are expected to increase their market share from 43.8% to 46.9% by 2029, reflecting a shift towards more advanced robotic systems.

Segment Analysis:

The medical vacuum systems market is divided into different types and applications, each catering to specific healthcare needs. Among the types, dry claw pump technology is becoming popular due to its ability to operate without oil, offering cleaner suction and lower maintenance. This technology is often used in hospitals for general suction purposes. Dry rotary vane technology is another type, providing reliable performance with reduced noise levels, making it ideal for sensitive environments like operating rooms and intensive care units. Oil-sealed rotary vane technology is more commonly used in high-demand settings like wound suction, where powerful and continuous suction is required for faster recovery and infection prevention. When it comes to applications, respiratory suction systems are widely used in emergency and intensive care units to clear airways, especially for patients with breathing difficulties. In gastric suction, these systems help in the removal of fluids, ensuring that the stomach remains free of harmful materials during surgeries. Wound suction, a critical application in post-operative care, helps in the prevention of infections and accelerates the healing process by removing fluids from surgical sites. In delivery rooms, vacuum systems are used during childbirth to assist in the extraction of fluids from the newborn's airways, promoting safe breathing.

Regional Analysis:

The global medical vacuum systems market is growing across various regions, each showing distinct trends and needs. In North America, the demand for advanced healthcare infrastructure drives the adoption of sophisticated vacuum systems in hospitals, particularly in critical care units and surgical theaters. The U.S. leads with extensive use in respiratory and wound suction applications. In Europe, high standards of healthcare and increasing awareness about infection control fuel the adoption of vacuum systems, particularly in hospitals and clinics that deal with complex surgical procedures. The growing elderly population in Europe also requires more intensive care, further driving demand. In the Asia-Pacific region, rapid urbanization and advancements in healthcare facilities are creating a strong demand for medical vacuum systems. Countries like China and India are increasingly investing in healthcare infrastructure, resulting in the expansion of hospitals and clinics requiring these systems for efficient patient care. The Middle East and Africa are witnessing a growing trend of medical infrastructure development, especially in countries like Saudi Arabia and the UAE, where healthcare reforms are being implemented. In Latin America, the rising number of surgeries and the expansion of healthcare services are driving the need for vacuum systems, particularly in Brazil and Mexico, where medical tourism is also contributing to market growth.

Competitive Scenario:

The medical vacuum systems market is characterized by diverse companies offering a range of products and services. Allied Healthcare Products, Inc. provides medical gas equipment, including vacuum systems, catering to various healthcare settings. Precision Medical, Inc. offers vacuum regulators and suction equipment, enhancing respiratory care in hospitals and clinics. Drive Medical supplies durable medical equipment, including portable suction units, facilitating patient mobility and care. INTEGRA Biosciences AG specializes in laboratory equipment, contributing to medical research and diagnostics. Medicop, Inc. manufactures medical devices, including suction systems, supporting surgical procedures and patient recovery. SSCOR, Inc. produces portable suction devices, essential for emergency medical services and patient transport. ATMOS MedizinTechnik GmbH & Co. KG offers medical suction systems, serving various applications from respiratory care to surgical suction. ZOLL Medical Corporation provides medical devices, including suction equipment, enhancing patient care in critical situations. Welch Vacuum manufactures vacuum pumps, supporting laboratory and medical applications with reliable suction solutions. Laerdal Medical focuses on training and resuscitation equipment, contributing to emergency medical education and preparedness. Labconco Corporation designs laboratory equipment, including vacuum systems, aiding in medical research and testing. Amsino International Inc. supplies medical devices, including suction equipment, supporting healthcare providers in various settings. Olympus Corporation offers medical instruments, including suction devices, enhancing diagnostic and therapeutic procedures. These companies collectively contribute to the advancement of medical vacuum systems, supporting healthcare professionals in delivering quality patient care.

Medical Vacuum Systems Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 6.1 Billion |

| Revenue Forecast in 2035 | USD 20.91 Billion |

| Growth Rate | CAGR of 11.84% from 2025 to 2035 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2035 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Allied Healthcare Products, Inc.; Precision Medical, Inc.; Drive Medical; INTEGRA Biosciences AG; Medicop, Inc.; SSCOR, Inc.; ATMOS MedizinTechnik GmbH & Co. KG; ZOLL Medical Corporation; Welch Vacuum; Laerdal Medical; Labconco Corporation; Amsino International Inc; Olympus Corporation |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Medical Vacuum Systems Market report is segmented as follows:

By Type,

- Dry Claw Pump Techology

- Dry Rotary Vane Technology

- Oil Sealed Rotary Vane Technology

By Application,

- Respiratory

- Gastric

- Wound Suction

- Delivery Room

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

Key Market Players,

- Allied Healthcare Products, Inc.

- Precision Medical, Inc.

- Drive Medical

- INTEGRA Biosciences AG

- Medicop, Inc.

- SSCOR, Inc.

- ATMOS MedizinTechnik GmbH & Co. KG

- ZOLL Medical Corporation

- Welch Vacuum

- Laerdal Medical

- Labconco Corporation

- Amsino International Inc

- Olympus Corporation

Frequently Asked Questions

How big is the Medical Vacuum Systems market?

Global Medical Vacuum Systems Market Size was valued at USD 6.1 Billion in 2024 and is projected to reach at USD 20.91 Billion in 2035.

What is the Medical Vacuum Systems market growth?

Global Medical Vacuum Systems Market is expected to grow at a CAGR of around 11.84% during the forecasted year.

Which region has the largest market share in Medical Vacuum Systems market?

North America, Asia Pacific and Europe are major regions in the global Medical Vacuum Systems Market.

Who are the key players in Medical Vacuum Systems market?

Key players analyzed in the global Medical Vacuum Systems Market are Allied Healthcare Products, Inc.; Precision Medical, Inc.; Drive Medical; INTEGRA Biosciences AG; Medicop, Inc.; SSCOR, Inc.; ATMOS MedizinTechnik GmbH & Co. KG; ZOLL Medical Corporation; Welch Vacuum; Laerdal Medical; Labconco Corporation; Amsino International Inc; Olympus Corporation and so on.