Global PVD/PAD Medical Device Market - Size and Forecast Analysis, 2021-2035

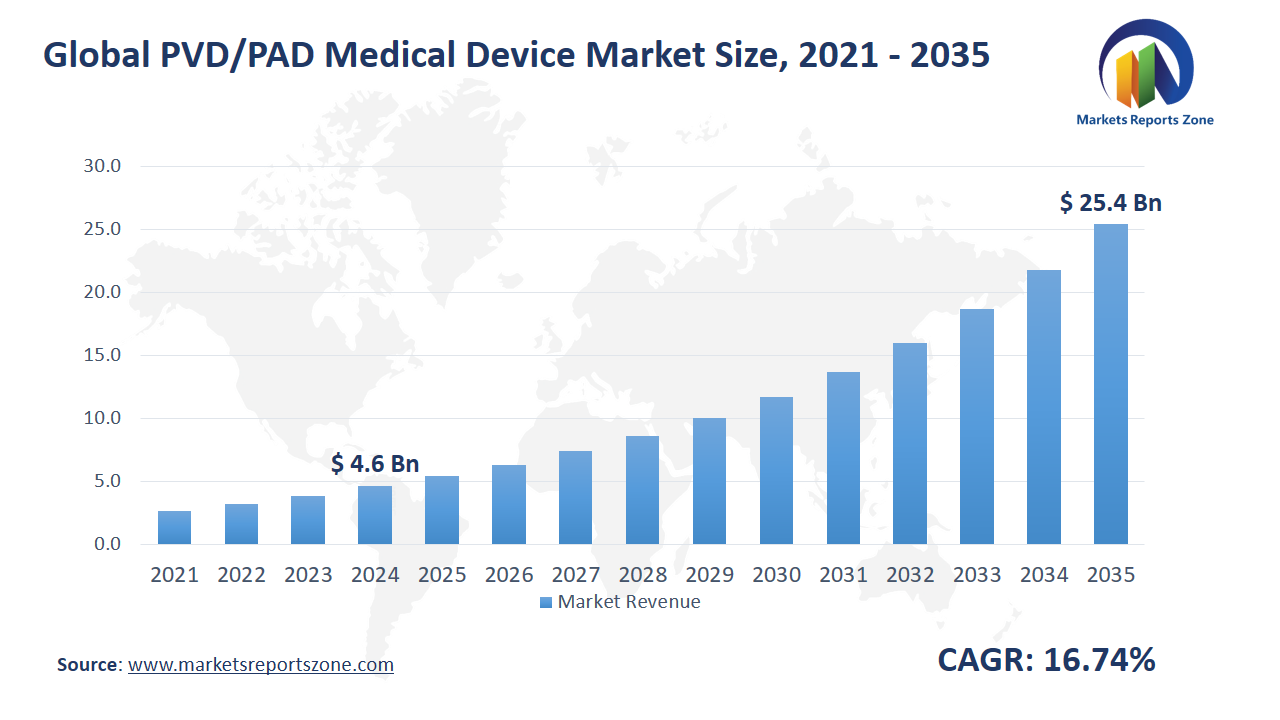

Global PVD/PAD Medical Device Market Size is expected to reach USD 25.47 Billion by 2035 from USD 4.63 Billion in 2024, with a CAGR of around 16.74% between 2024 and 2035. The global PVD/PAD medical device market is driven by rising cases of peripheral vascular disease and increasing demand for minimally invasive treatments. Aging populations and sedentary lifestyles are contributing to a higher prevalence of PVD, boosting the need for effective medical devices. Minimally invasive procedures are being preferred by patients and healthcare providers due to reduced recovery time and lower risks. However, high costs of advanced PVD/PAD devices and procedures are acting as a major restraint, limiting their accessibility, especially in low-income regions. Despite this, opportunities are emerging with technological advancements in device design and material innovation. Next-generation stents and drug-coated balloons are being developed to improve treatment outcomes. Additionally, increasing government initiatives and healthcare investments are creating growth prospects. For example, Boston Scientific’s Ranger Drug-Coated Balloon is being used for PVD treatment with better long-term results. Medtronic’s IN.PACT Admiral drug-coated balloon is being deployed for femoropopliteal artery disease, enhancing patient care. With growing clinical trials and regulatory approvals, the market is expanding, offering new possibilities for improved PVD/PAD management. Continuous innovation and increased awareness are expected to further drive the adoption of advanced devices globally.

Driver: Rising PVD Cases Driving Device Demand

The growing prevalence of peripheral vascular disease (PVD) is significantly driving the demand for advanced medical devices. Sedentary lifestyles, poor dietary habits, and rising obesity rates are contributing to increased PVD cases worldwide. Aging populations are also more prone to developing vascular issues, leading to a higher need for effective treatment solutions. As a result, healthcare providers are increasingly relying on innovative PVD devices such as stents, drug-coated balloons, and atherectomy systems to manage the condition. For instance, Philips’ Stellarex drug-coated balloon is being used to treat femoropopliteal artery disease, offering better patency rates and reducing the need for repeat procedures. In addition, Cardiovascular Systems Inc. has introduced orbital atherectomy systems designed to remove plaque in calcified arteries, improving blood flow and reducing symptoms. Minimally invasive devices are being increasingly adopted due to their effectiveness in lowering complications and recovery times. With PVD cases on the rise, device manufacturers are focusing on developing more durable and efficient products. As patient awareness increases and early diagnosis rates improve, the demand for advanced PVD treatment devices is expected to grow, making them essential tools in managing the condition effectively.

Key Insights:

- The adoption rate of Peripheral Vascular Devices (PVD) in hospitals is approximately 35%, reflecting their critical role in treating cardiovascular conditions.

- Government funding for research and development in PAD medical devices reached around $300 million in 2024, emphasizing the importance of innovation in this field.

- In 2023, approximately 10,000 units of PAD-related medical devices were sold globally, indicating a growing market demand.

- The penetration rate of PVD in the cardiology sector is estimated to be around 40%, driven by the increasing prevalence of cardiovascular diseases.

- In 2024, major companies invested about $150 million in clinical trials aimed at improving PAD treatment technologies.

- The number of new PAD devices approved by regulatory agencies increased by 20% from 2022 to 2023, showcasing advancements in medical technology.

- Research indicates that approximately 25% of healthcare facilities are currently utilizing PVD technology to enhance patient outcomes in vascular treatments.

- By the end of 2025, it is projected that PVDs will account for over 30% of the total devices used in interventional cardiology procedures.

Segment Analysis:

The global PVD/PAD medical device market is segmented by type into peripheral vascular stents, PTA balloon catheters, PTA guidewires, atherectomy devices, and chronic total occlusion (CTO) devices. Peripheral vascular stents are being widely used to restore blood flow in narrowed or blocked arteries. Their ability to prevent restenosis is making them essential in long-term PVD treatment. Cook Medical’s Zilver PTX drug-eluting stent is being used to treat femoropopliteal disease, reducing reintervention rates. PTA balloon catheters are being increasingly adopted for minimally invasive angioplasty procedures, allowing effective vessel dilation. Biotronik’s Passeo-18 Lux is being deployed for treating peripheral artery lesions. PTA guidewires are enabling precise catheter placement during complex procedures, improving surgical outcomes. Atherectomy devices are being used to remove plaque buildup, ensuring better blood flow. Spectranetics’ Turbo-Power Laser Atherectomy Catheter is being utilized to treat heavily calcified arteries. CTO devices are addressing complex chronic blockages by facilitating safe and effective lesion crossing. By application, these devices are being used across various treatments, including peripheral artery disease management, limb preservation, and post-surgical care. With continuous technological advancements, these segments are playing a crucial role in enhancing PVD treatment outcomes and improving patient recovery rates.

Regional Analysis:

The global PVD/PAD medical device market is expanding across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America is leading due to the rising prevalence of peripheral vascular diseases and advanced healthcare infrastructure. In the U.S., innovative devices like Abbott’s Supera stent are being widely used for treating complex vascular conditions, reducing restenosis rates. Europe is witnessing increased adoption of minimally invasive procedures, with hospitals deploying Terumo’s Ultimaster stent for better patient outcomes. The Asia-Pacific region is growing rapidly due to improving healthcare systems and rising PVD awareness. In India, local hospitals are using Meril’s BioMime stent for cost-effective PAD treatment. Latin America is gradually adopting advanced devices, with healthcare providers in Brazil using Biosensors’ BioFreedom stent for drug-coated interventions. The Middle East & Africa region is experiencing moderate growth, driven by increasing healthcare investments. In Saudi Arabia, hospitals are deploying Boston Scientific’s Jetstream atherectomy system to treat calcified lesions effectively. Across all regions, rising patient awareness, technological advancements, and government initiatives are driving the adoption of PVD/PAD devices. With continuous innovation and better treatment options, the market is expanding globally, improving patient outcomes and reducing complications.

Competitive Scenario:

Leading companies in the PVD/PAD medical device market are driving growth through technological advancements, strategic collaborations, and innovative product launches. Gore is expanding its vascular device portfolio by introducing advanced stent grafts designed to improve long-term patency. Boston Scientific is enhancing its PVD treatment solutions by launching next-generation drug-coated balloons, offering better outcomes for complex lesions. FierceBiotech is collaborating with emerging medtech startups to develop cutting-edge vascular technologies. Medtronic is advancing its peripheral artery disease solutions by integrating artificial intelligence into its diagnostic and treatment devices. C.R. Bard, now part of BD, is expanding its product line with enhanced angioplasty catheters for improved precision during procedures. Johnson & Johnson is focusing on minimally invasive PVD treatments by investing in bioresorbable stent technologies. Abbott Laboratories is scaling its operations with drug-eluting stents that reduce restenosis risks, enhancing patient care. Angioscore Inc. is introducing scoring balloon catheters that offer superior vessel preparation capabilities. Edward Lifesciences Corporation is developing vascular monitoring solutions to optimize PVD management. Teleflex Medical is innovating with catheter-based solutions to improve procedural efficiency. St. Jude Medical is integrating smart technologies into vascular devices, while Volcano Corporation, part of Philips, is advancing intravascular imaging solutions. Cook Group Inc., Cordis Corporation, Bayer, and Endologix are continuously innovating with next-generation vascular devices, improving PVD treatment outcomes.

PVD/PAD Medical Device Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 4.63 Billion |

| Revenue Forecast in 2035 | USD 25.47 Billion |

| Growth Rate | CAGR of 16.74% from 2025 to 2035 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2035 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Gore; Boston Scientific; FierceBiotech; Medtronic; C.R.Bard; Johnson & Johnson; Abbott Laboratories; Angioscore Inc.; Edward Lifesciences Corporation; Teleflex Medical; St. Jude Medical; Volcano Corporation; Cook Group Inc.; Cordis Corporation; Bayer; Endologix |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global PVD/PAD Medical Device Market report is segmented as follows:

By Type,

- Peripheral vascular stents

- Peripheral transluminal angioplasty balloon catheters

- PTA guidewires

- Atherectomy devices

- Chronic total occlusion devices

By Application,

- Application 1

- Application 2

- Application 3

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

Key Market Players,

- Gore

- Boston Scientific

- FierceBiotech

- Medtronic

- C.R.Bard

- Johnson & Johnson

- Abbott Laboratories

- Angioscore Inc.

- Edward Lifesciences Corporation

- Teleflex Medical

- St. Jude Medical

- Volcano Corporation

- Cook Group Inc.

- Cordis Corporation

- Bayer

- Endologix

Frequently Asked Questions

How big is the PVD/PAD Medical Device Market market?

Global PVD/PAD Medical Device Market Size was valued at USD 4.63 Billion in 2024 and is projected to reach at USD 25.47 Billion in 2035.

What is the PVD/PAD Medical Device Market market growth?

Global PVD/PAD Medical Device Market is expected to grow at a CAGR of around 16.74% during the forecasted year.

Which region has the largest market share in PVD/PAD Medical Device Market market?

North America, Asia Pacific and Europe are major regions in the global PVD/PAD Medical Device Market.

Who are the key players in PVD/PAD Medical Device Market market?

Key players analyzed in the global PVD/PAD Medical Device Market are Gore; Boston Scientific; FierceBiotech; Medtronic; C.R.Bard; Johnson & Johnson; Abbott Laboratories; Angioscore Inc.; Edward Lifesciences Corporation; Teleflex Medical; St. Jude Medical; Volcano Corporation; Cook Group Inc.; Cordis Corporation; Bayer; Endologix and so on.