Global Power invertor Market - Size and Forecast Analysis, 2021-2035

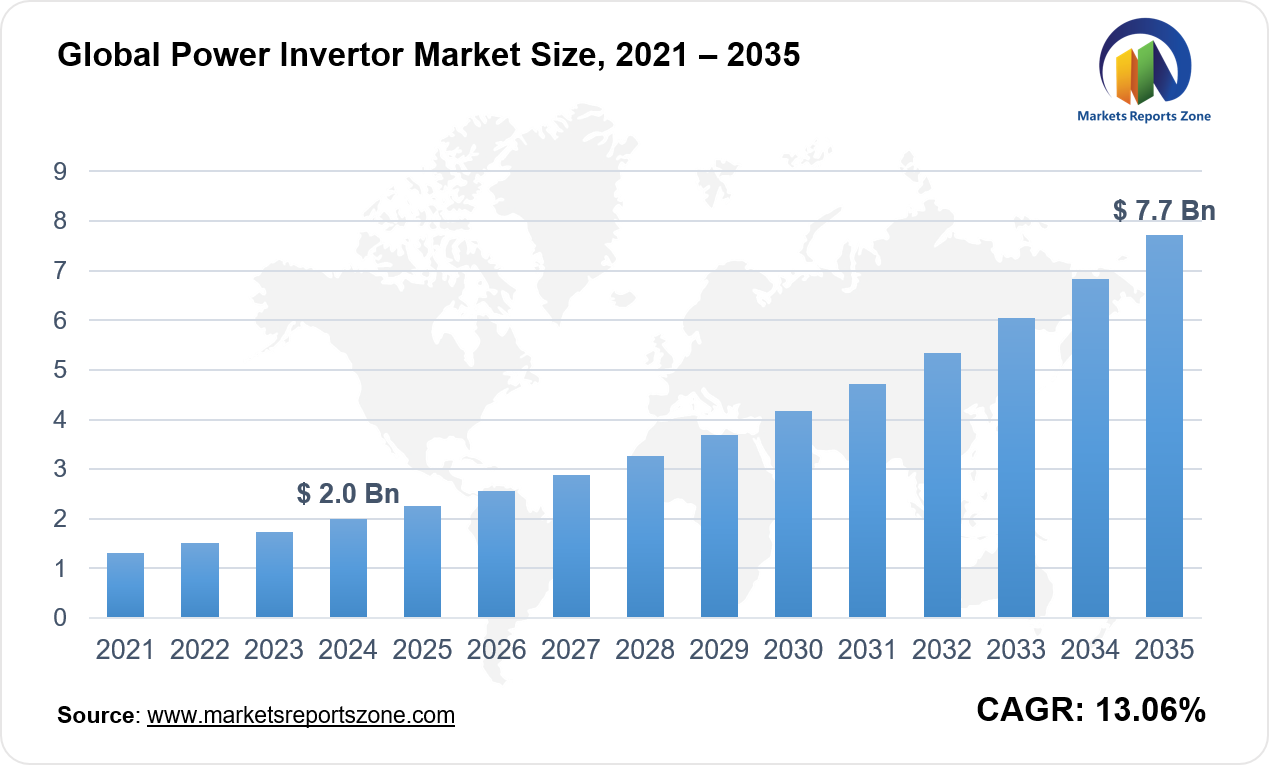

Global Power invertor Market Size is expected to reach USD 7.75 Billion by 2035 from USD 2 Billion in 2024, with a CAGR of around 13.06% between 2024 and 2035. The global power inverter market is being driven by the rising demand for renewable energy solutions and the growing need for uninterrupted power supply. Increasing solar panel installations in residential and commercial sectors are fueling market growth. The rising adoption of electric vehicles (EVs) is further boosting inverter demand, as efficient power conversion is required for vehicle charging stations. However, market expansion is being restrained by the high initial investment costs associated with advanced inverters. Despite this, new opportunities are emerging. The increasing integration of smart inverters with Internet of Things (IoT) capabilities is creating growth potential. These smart inverters are being widely used in remote monitoring and energy management systems. Additionally, the surging demand for portable inverters in outdoor activities and emergency power backup is driving new business prospects. For instance, portable inverters are being increasingly used in camping trips and construction sites for reliable power access. Furthermore, smart inverters are being implemented in smart homes to optimize energy usage. With the continuous focus on sustainable energy and technological advancements, the power inverter market is expected to witness steady growth.

Driver: Solar Power Surge Boosting Inverter Demand

The increasing adoption of solar energy is driving the demand for power inverters globally. As more households and businesses switch to solar panels, efficient energy conversion becomes essential. Power inverters play a crucial role in converting DC power from solar panels into usable AC electricity. Governments are actively promoting solar installations through incentives and subsidies, further accelerating market growth. In urban areas, high-rise buildings are increasingly integrating solar panels with inverters to reduce dependence on conventional grids. Rural regions are also benefiting, where solar-powered inverters are being used to electrify remote villages. Large-scale solar farms are deploying advanced inverters to enhance grid stability and optimize energy distribution. Homeowners are opting for hybrid inverters to store excess solar energy in batteries, ensuring power availability during outages. In the agricultural sector, solar-powered inverters are being used to run irrigation pumps, reducing reliance on diesel generators. Businesses are also installing solar inverters to cut electricity costs and achieve sustainability goals. With the rising focus on clean energy and energy independence, the demand for efficient power inverters is expected to grow rapidly, making them a vital component in the global shift toward renewable energy solutions.

Key Insights:

- The adoption rate of power inverters in renewable energy systems has reached approximately 45% globally, driven by increasing investments in solar and wind energy.

- In 2023, government investments in renewable energy projects, which include power inverter technologies, totaled around $30 billion across various countries to promote clean energy initiatives.

- The number of power inverters sold globally in 2024 is estimated to be around 25 million units, reflecting a significant increase due to rising demand for renewable energy solutions.

- The penetration rate of power inverters among industrial applications is reported to be about 60%, as industries seek efficient energy management systems.

- In 2024, the utility sector accounted for approximately 70% of all power inverter installations, highlighting its critical role in large-scale renewable energy projects.

- The average investment by companies in developing advanced inverter technologies was around $5 billion in 2023, focusing on improving efficiency and integration with smart grid systems.

- Approximately 35% of residential households have adopted power inverter systems as backup solutions to ensure uninterrupted power supply during outages.

- The global market for power inverters is projected to grow at a rate of about 8% annually, reflecting the ongoing transition towards sustainable energy sources and technological advancements.

Segment Analysis:

The global power inverter market is expanding across various segments, driven by diverse applications. Current source inverters (CSIs) are being widely used in industrial drives due to their ability to handle high currents with consistent performance. In large manufacturing plants, CSIs are powering heavy machinery, improving operational efficiency. On the other hand, voltage source inverters (VSIs) are dominating renewable energy systems due to their fast switching capabilities and stable output. In photovoltaic (PV) systems, VSIs are being deployed to efficiently convert solar energy into usable electricity. Residential buildings are increasingly installing PV inverters to reduce reliance on grid power and lower energy bills. In wind energy systems, VSIs are enabling seamless power conversion, ensuring smooth energy transmission to the grid. In remote areas, wind farms are leveraging these inverters to supply stable power to local communities. The industrial drive segment is also witnessing strong growth, with inverters being used to control motor speeds and enhance energy efficiency in factories. In agricultural applications, inverters are driving water pumps for irrigation, helping farmers reduce fuel costs. With the rising focus on sustainability and energy efficiency, the demand for reliable power inverters across these segments is steadily increasing.

Regional Analysis:

The power inverter market is witnessing significant growth across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, driven by increasing energy demands and renewable adoption. In North America, rising investments in solar farms are fueling inverter demand, with businesses integrating hybrid inverters for uninterrupted power supply. Smart home adoption is also boosting inverter installations for energy-efficient solutions. In Europe, strict carbon reduction policies are driving the shift to renewable energy, leading to widespread deployment of inverters in residential and commercial solar projects. Countries like Germany and France are expanding EV charging infrastructure, increasing demand for high-efficiency inverters. The Asia-Pacific region is seeing rapid industrialization, with inverters powering factory automation and grid stability in countries like China and India. Large-scale wind and solar projects are utilizing advanced inverters to optimize power generation. In Latin America, rural electrification projects are driving inverter adoption, particularly in off-grid solar systems for remote communities. Agricultural applications, such as solar-powered irrigation, are also gaining traction. In the Middle East & Africa, demand for solar inverters is surging due to extreme temperatures and unreliable grid power, with solar farms supplying electricity to isolated regions. The global push for clean energy is accelerating inverter adoption across all regions.

Competitive Scenario:

Leading companies in the global power inverter market are driving innovation and expanding their portfolios to meet growing energy demands. SMA, ABB, and SolarEdge are enhancing their inverter technologies with improved efficiency and smart grid integration. Recently, Enphase Energy introduced advanced microinverters with faster power conversion, catering to residential and commercial solar projects. Huawei and Sungrow Power are focusing on large-scale solar farms, offering high-capacity string inverters for optimized energy output. Siemens and Danfoss are expanding their industrial inverter solutions, targeting manufacturing plants with advanced motor control capabilities. Fronius and KACO are strengthening their presence in the European market by launching hybrid inverters, addressing the rising demand for solar-plus-storage systems. Power Electronics and Growatt are making strides in the EV sector, introducing inverters for charging infrastructure to support the growing electric vehicle market. Chint and TBEA are increasingly supplying inverters to large-scale renewable projects in Asia, boosting grid stability. Additionally, Schneider Electric and Advanced Energy are incorporating IoT-enabled monitoring in their inverters, allowing real-time performance tracking. With ongoing technological advancements and a focus on renewable energy integration, these companies are playing a key role in shaping the future of the power inverter market.

Power invertor Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 2 Billion |

| Revenue Forecast in 2035 | USD 7.75 Billion |

| Growth Rate | CAGR of 13.06% from 2025 to 2035 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2035 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | SMA; ABB; AdvancedEnergy; EnphaseEnergy; SolarEdge; SchnriderElectric; Power Electronics; Fronius; Power-One; KACO; Ingeteam; Siemens; Danfoss; Kostal; TBEA; HuaWei; KSTAR; Chint; Sungrowpower; Zeversolar; Growatt; Beijing NeGo; Anhui EHE; Omnik |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global Power invertor Market report is segmented as follows:

By Type,

- Current Source invertor

- Voltage Source invertor

By Application,

- Industrial drives

- Photovoltaic (PV) systems

- Wind energy systems

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

Key Market Players,

- SMA

- ABB

- AdvancedEnergy

- EnphaseEnergy

- SolarEdge

- SchnriderElectric

- Power Electronics

- Fronius

- Power-One

- KACO

- Ingeteam

- Siemens

- Danfoss

- Kostal

- TBEA

- HuaWei

- KSTAR

- Chint

- Sungrowpower

- Zeversolar

- Growatt

- Beijing NeGo

- Anhui EHE

- Omnik

Frequently Asked Questions

How big is the Power invertor Market market?

Global Power invertor Market Size was valued at USD 2 Billion in 2024 and is projected to reach at USD 7.75 Billion in 2035.

What is the Power invertor Market market growth?

Global Power invertor Market is expected to grow at a CAGR of around 13.06% during the forecasted year.

Which region has the largest market share in Power invertor Market market?

North America, Asia Pacific and Europe are major regions in the global Power invertor Market.

Who are the key players in Power invertor Market market?

Key players analyzed in the global Power invertor Market are SMA; ABB; AdvancedEnergy; EnphaseEnergy; SolarEdge; SchnriderElectric; Power Electronics; Fronius; Power-One; KACO; Ingeteam; Siemens; Danfoss; Kostal; TBEA; HuaWei; KSTAR; Chint; Sungrowpower; Zeversolar; Growatt; Beijing NeGo; Anhui EHE; Omnik and so on.