Global The Food Market, By Type (By Product, Search Heads, Conveyor based Systems, Pipeline for Pumped Products, Vertical Fall or Gravity Feed), By Application, and By Region - Trends and Forecast Analysis, 2021-2035

Publish Date: 2025-03-23 | Format: PDF | Category: Machinery and Equipment | Pages: 300

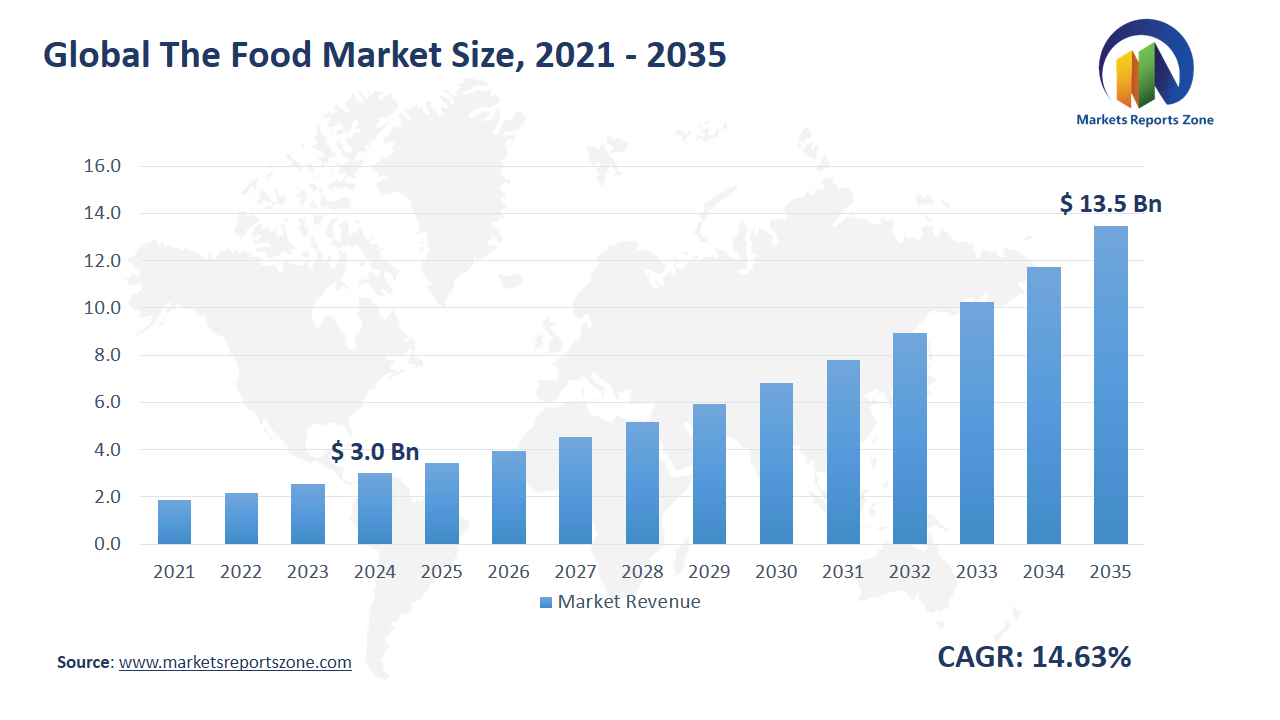

Global The Food Market Size is expected to reach USD 13.48 Billion by 2035 from USD 3 Billion in 2024, with a CAGR of around 14.63% between 2024 and 2035. Rising consumer demand for healthy food and the expansion of e-commerce have been driving the global food market. People are becoming more health-conscious, leading to a surge in organic, plant-based, and functional food products. Large supermarket chains and food brands have been introducing gluten-free, vegan, and high-protein options to cater to shifting preferences. The growth of online food delivery services has also been transforming the market. Digital platforms have been enabling quick access to fresh produce, ready-to-eat meals, and specialty foods, even in remote areas. However, supply chain disruptions have been a major restraint. Delays in transportation, labor shortages, and rising raw material costs have been affecting food production and distribution. Despite these challenges, new opportunities have been emerging. The adoption of sustainable packaging has been gaining momentum as companies focus on reducing plastic waste. Biodegradable materials and reusable containers have been replacing traditional packaging in major food brands. Additionally, the rise of alternative proteins has been creating new possibilities. Companies have been investing in lab-grown meat, insect-based proteins, and plant-based substitutes to address environmental concerns and meet growing consumer demand. With continued innovation, the food industry has been evolving to ensure affordability, sustainability, and convenience for global consumers.

Driver: Health-Conscious Choices Reshaping Food Industry

Growing awareness of nutrition has been driving major changes in the food market. Consumers have been actively seeking healthier alternatives, leading to a rise in organic, plant-based, and functional foods. Fast food chains have been introducing low-calorie, high-protein, and plant-based menu options to cater to changing preferences. In supermarkets, shelves have been stocked with gluten-free, dairy-free, and sugar-free products to meet increasing demand. Food brands have been reformulating products by reducing artificial ingredients and fortifying them with vitamins, minerals, and probiotics. The trend has also been impacting the beverage industry. Cold-pressed juices, kombucha, and plant-based milk alternatives have been growing in popularity. Even traditional snack manufacturers have been shifting towards protein bars, baked chips, and natural fruit-based treats. Restaurants have been adjusting their menus to include whole grains, organic produce, and ethically sourced ingredients. Meal kit delivery services have been providing customers with fresh, portion-controlled meals designed for specific dietary needs. Fitness influencers and nutritionists have been further promoting clean eating habits through social media, reinforcing the shift toward better food choices. As health remains a priority, the food industry has been rapidly evolving to align with consumer expectations for better nutrition and well-being.

Key Insights:

- The adoption rate of innovative food technologies in the food market is approximately 38% as of 2024.

- Investments by companies and governments in food technology advancements have reached around $500 million in recent years.

- In 2023, an estimated 3 million tons of various food products were sold globally through advanced distribution channels.

- The penetration rate of online food delivery services in urban areas is about 55%, reflecting a significant shift in consumer purchasing behavior.

- Approximately 65% of restaurants are integrating technology solutions to enhance customer experience and streamline operations.

- The annual growth rate for investments in sustainable food production technologies is projected to be around 10% over the next five years.

- Surveys indicate that nearly 70% of consumers are willing to pay a premium for organic and locally sourced food products.

- The market is experiencing increased demand for plant-based food options, with expectations of a 20% annual growth in sales through 2026.

Segment Analysis:

Metal detection systems have been playing a crucial role in the food industry, ensuring safety and compliance across various product categories. Search heads have been widely used in packaging lines to detect contaminants in bakery goods, preventing foreign objects from reaching consumers. Conveyor-based systems have been essential in dairy production, scanning milk cartons and yogurt containers for any traces of metal. Pipeline systems for pumped products have been ensuring the purity of liquid-based foods, such as soups and sauces, by identifying even the smallest metal fragments. Vertical fall or gravity feed systems have been integrated into fruit and vegetable processing plants, where they check dried fruits, nuts, and grains for any potential contamination before packaging. In the ready-meals sector, metal detectors have been installed at multiple points in production to inspect frozen dinners and microwaveable meals. Fish and seafood processing plants have been relying on advanced detection systems to maintain the highest safety standards, particularly in deboned and processed products. With rising consumer awareness and stricter regulations, food manufacturers have been continuously upgrading their metal detection technology to minimize risks and maintain brand trust. These innovations have been crucial in preventing recalls and protecting public health.

Regional Analysis:

Metal detection systems have been implemented worldwide to ensure food safety across different regions. In North America, large-scale food manufacturers have been using advanced conveyor-based metal detectors to inspect packaged snacks, reducing contamination risks. In Europe, strict food safety regulations have led dairy producers to adopt pipeline metal detection systems, ensuring milk and cheese remain free from metal particles. The Asia-Pacific region has seen a surge in demand for gravity-feed metal detectors in rice and grain processing plants, preventing foreign object contamination before distribution. In Latin America, the seafood industry has relied on high-sensitivity metal detectors to inspect fish fillets and canned seafood, maintaining export standards. The Middle East and Africa have seen increased adoption of search head detectors in ready-meal production, ensuring processed foods remain free from contaminants before reaching consumers. As food exports grow and global safety regulations become stricter, companies have been investing in cutting-edge detection technologies to maintain product integrity. Industries worldwide have recognized the importance of minimizing recalls and protecting brand reputation by implementing reliable metal detection systems. With continuous advancements, food producers in all regions have been upgrading their systems to meet evolving safety standards and consumer expectations.

Competitive Scenario:

Leading companies in the metal detection industry have been innovating to enhance food safety and efficiency in production. Mettler-Toledo and Thermo Fisher have been integrating AI-driven detection technology, improving sensitivity to even the smallest metal contaminants in dairy and baked goods. Eriez and Sesotec have been expanding their conveyor-based systems, ensuring seamless inspection in high-speed food processing lines. CEIA and Loma have introduced advanced search head systems that offer multi-frequency detection, increasing accuracy across various food products. Anritsu and VinSyst have focused on compact metal detectors for small-scale manufacturers, making high-end detection accessible to local food producers. Foremost and COSO have developed high-speed pipeline metal detection systems for liquid and pumped products, preventing contamination in sauces and dairy processing. Lock Inspection and Nikka Densok have been refining vertical fall and gravity-feed metal detectors, optimizing quality control in grain and snack food production. Cassel Messtechnik has been launching energy-efficient detection units, helping manufacturers reduce operational costs while maintaining strict food safety standards. As regulatory requirements tighten worldwide, companies have been prioritizing automation, digital monitoring, and real-time reporting, ensuring that food processors can meet safety expectations while maintaining high production efficiency.

The Food Market Report Scope

| Report Attribute | Details |

|---|---|

| Market Size Value in 2024 | USD 3 Billion |

| Revenue Forecast in 2035 | USD 13.48 Billion |

| Growth Rate | CAGR of 14.63% from 2025 to 2035 |

| Historic Period | 2021 - 2024 |

| Forecasted Period | 2025 - 2035 |

| Report Coverage | Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

| Regions Covered | North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Countries Covered | U.S.; Canada; Mexico, UK; Germany; France; Spain; Italy; Russia; China; Japan; India; South Korea; Australia; Southeast Asia; Brazil; Argentina; Saudi Arabia; UAE; South Africa |

| Key companies profiled | Mettler-Toledo; Eriez; CEIA; Loma; Anritsu; VinSyst; Foremost; COSO; Sesotec; Metal Detection; Thermo Fisher; Lock Inspection; Nikka Densok; Cassel Messtechnik |

| Customization | Free report customization (equivalent up to 8 analysts working days) with purchase. Addition or alteration to country, regional & segment scope. |

The Global The Food Market report is segmented as follows:

By Type,

- By Product

- Search Heads

- Conveyor based Systems

- Pipeline for Pumped Products

- Vertical Fall or Gravity Feed

By Application,

- Bakery or Baked Goods

- Dairy, Milk, Yoghurt

- Fruit and Vegetables

- Ready Meals

- Fish and Seafood

By Region,

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of Middle East and Africa

Key Market Players,

- Mettler-Toledo

- Eriez

- CEIA

- Loma

- Anritsu

- VinSyst

- Foremost

- COSO

- Sesotec

- Metal Detection

- Thermo Fisher

- Lock Inspection

- Nikka Densok

- Cassel Messtechnik

Frequently Asked Questions

Research Objectives

- Proliferation and maturation of trade in the global The Food Market.

- The market share of the global The Food Market, supply and demand ratio, growth revenue, supply chain analysis, and business overview.

- Current and future market trends that are influencing the growth opportunities and growth rate of the global The Food Market.

- Feasibility study, new market insights, company profiles, investment return, market size of the global The Food Market.

Chapter 1 The Food Market Executive Summary

- 1.1 The Food Market Research Scope

- 1.2 The Food Market Estimates and Forecast (2021-2035)

- 1.2.1 Global The Food Market Value and Growth Rate (2021-2035)

- 1.2.2 Global The Food Market Price Trend (2021-2035)

- 1.3 Global The Food Market Value Comparison, by Type (2021-2035)

- 1.3.1 By Product

- 1.3.2 Search Heads

- 1.3.3 Conveyor based Systems

- 1.3.4 Pipeline for Pumped Products

- 1.3.5 Vertical Fall or Gravity Feed

- 1.4 Global The Food Market Value Comparison, by Application (2021-2035)

- 1.4.1 Bakery or Baked Goods

- 1.4.2 Dairy, Milk, Yoghurt

- 1.4.3 Fruit and Vegetables

- 1.4.4 Ready Meals

- 1.4.5 Fish and Seafood

Chapter 2 Research Methodology

- 2.1 Introduction

- 2.2 Data Capture Sources

- 2.2.1 Primary Sources

- 2.2.2 Secondary Sources

- 2.3 Market Size Estimation

- 2.4 Market Forecast

- 2.5 Assumptions and Limitations

Chapter 3 Market Dynamics

- 3.1 Market Trends

- 3.2 Opportunities and Drivers

- 3.3 Challenges

- 3.4 Market Restraints

- 3.5 Porter's Five Forces Analysis

Chapter 4 Supply Chain Analysis and Marketing Channels

- 4.1 The Food Supply Chain Analysis

- 4.2 Marketing Channels

- 4.3 The Food Suppliers List

- 4.4 The Food Distributors List

- 4.5 The Food Customers

Chapter 5 COVID-19 & Russia?Ukraine War Impact Analysis

- 5.1 COVID-19 Impact Analysis on The Food Market

- 5.2 Russia-Ukraine War Impact Analysis on The Food Market

Chapter 6 The Food Market Estimate and Forecast by Region

- 6.1 Global The Food Market Value by Region: 2021 VS 2023 VS 2035

- 6.2 Global The Food Market Scenario by Region (2021-2023)

- 6.2.1 Global The Food Market Value Share by Region (2021-2023)

- 6.3 Global The Food Market Forecast by Region (2024-2035)

- 6.3.1 Global The Food Market Value Forecast by Region (2024-2035)

- 6.4 Geographic Market Analysis: Market Facts and Figures

- 6.4.1 North America The Food Market Estimates and Projections (2021-2035)

- 6.4.2 Europe The Food Market Estimates and Projections (2021-2035)

- 6.4.3 Asia Pacific The Food Market Estimates and Projections (2021-2035)

- 6.4.4 Latin America The Food Market Estimates and Projections (2021-2035)

- 6.4.5 Middle East & Africa The Food Market Estimates and Projections (2021-2035)

Chapter 7 Global The Food Competition Landscape by Players

- 7.1 Global Top The Food Players by Value (2021-2023)

- 7.2 The Food Headquarters and Sales Region by Company

- 7.3 Company Recent Developments, Mergers & Acquisitions, and Expansion Plans

Chapter 8 Global The Food Market, by Type

- 8.1 Global The Food Market Value, by Type (2021-2035)

- 8.1.1 By Product

- 8.1.2 Search Heads

- 8.1.3 Conveyor based Systems

- 8.1.4 Pipeline for Pumped Products

- 8.1.5 Vertical Fall or Gravity Feed

Chapter 9 Global The Food Market, by Application

- 9.1 Global The Food Market Value, by Application (2021-2035)

- 9.1.1 Bakery or Baked Goods

- 9.1.2 Dairy, Milk, Yoghurt

- 9.1.3 Fruit and Vegetables

- 9.1.4 Ready Meals

- 9.1.5 Fish and Seafood

Chapter 10 North America The Food Market

- 10.1 Overview

- 10.2 North America The Food Market Value, by Country (2021-2035)

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 North America The Food Market Value, by Type (2021-2035)

- 10.3.1 By Product

- 10.3.2 Search Heads

- 10.3.3 Conveyor based Systems

- 10.3.4 Pipeline for Pumped Products

- 10.3.5 Vertical Fall or Gravity Feed

- 10.4 North America The Food Market Value, by Application (2021-2035)

- 10.4.1 Bakery or Baked Goods

- 10.4.2 Dairy, Milk, Yoghurt

- 10.4.3 Fruit and Vegetables

- 10.4.4 Ready Meals

- 10.4.5 Fish and Seafood

Chapter 11 Europe The Food Market

- 11.1 Overview

- 11.2 Europe The Food Market Value, by Country (2021-2035)

- 11.2.1 UK

- 11.2.2 Germany

- 11.2.3 France

- 11.2.4 Spain

- 11.2.5 Italy

- 11.2.6 Russia

- 11.2.7 Rest of Europe

- 11.3 Europe The Food Market Value, by Type (2021-2035)

- 11.3.1 By Product

- 11.3.2 Search Heads

- 11.3.3 Conveyor based Systems

- 11.3.4 Pipeline for Pumped Products

- 11.3.5 Vertical Fall or Gravity Feed

- 11.4 Europe The Food Market Value, by Application (2021-2035)

- 11.4.1 Bakery or Baked Goods

- 11.4.2 Dairy, Milk, Yoghurt

- 11.4.3 Fruit and Vegetables

- 11.4.4 Ready Meals

- 11.4.5 Fish and Seafood

Chapter 12 Asia Pacific The Food Market

- 12.1 Overview

- 12.2 Asia Pacific The Food Market Value, by Country (2021-2035)

- 12.2.1 China

- 12.2.2 Japan

- 12.2.3 India

- 12.2.4 South Korea

- 12.2.5 Australia

- 12.2.6 Southeast Asia

- 12.2.7 Rest of Asia Pacific

- 12.3 Asia Pacific The Food Market Value, by Type (2021-2035)

- 12.3.1 By Product

- 12.3.2 Search Heads

- 12.3.3 Conveyor based Systems

- 12.3.4 Pipeline for Pumped Products

- 12.3.5 Vertical Fall or Gravity Feed

- 12.4 Asia Pacific The Food Market Value, by Application (2021-2035)

- 12.4.1 Bakery or Baked Goods

- 12.4.2 Dairy, Milk, Yoghurt

- 12.4.3 Fruit and Vegetables

- 12.4.4 Ready Meals

- 12.4.5 Fish and Seafood

Chapter 13 Latin America The Food Market

- 13.1 Overview

- 13.2 Latin America The Food Market Value, by Country (2021-2035)

- 13.2.1 Brazil

- 13.2.2 Argentina

- 13.2.3 Rest of Latin America

- 13.3 Latin America The Food Market Value, by Type (2021-2035)

- 13.3.1 By Product

- 13.3.2 Search Heads

- 13.3.3 Conveyor based Systems

- 13.3.4 Pipeline for Pumped Products

- 13.3.5 Vertical Fall or Gravity Feed

- 13.4 Latin America The Food Market Value, by Application (2021-2035)

- 13.4.1 Bakery or Baked Goods

- 13.4.2 Dairy, Milk, Yoghurt

- 13.4.3 Fruit and Vegetables

- 13.4.4 Ready Meals

- 13.4.5 Fish and Seafood

Chapter 14 Middle East & Africa The Food Market

- 14.1 Overview

- 14.2 Middle East & Africa The Food Market Value, by Country (2021-2035)

- 14.2.1 Saudi Arabia

- 14.2.2 UAE

- 14.2.3 South Africa

- 14.2.4 Rest of Middle East & Africa

- 14.3 Middle East & Africa The Food Market Value, by Type (2021-2035)

- 14.3.1 By Product

- 14.3.2 Search Heads

- 14.3.3 Conveyor based Systems

- 14.3.4 Pipeline for Pumped Products

- 14.3.5 Vertical Fall or Gravity Feed

- 14.4 Middle East & Africa The Food Market Value, by Application (2021-2035)

- 14.4.1 Bakery or Baked Goods

- 14.4.2 Dairy, Milk, Yoghurt

- 14.4.3 Fruit and Vegetables

- 14.4.4 Ready Meals

- 14.4.5 Fish and Seafood

Chapter 15 Company Profiles and Market Share Analysis: (Business Overview, Market Share Analysis, Products/Services Offered, Recent Developments)

- 15.1 Mettler-Toledo

- 15.2 Eriez

- 15.3 CEIA

- 15.4 Loma

- 15.5 Anritsu

- 15.6 VinSyst

- 15.7 Foremost

- 15.8 COSO

- 15.9 Sesotec

- 15.10 Metal Detection

- 15.11 Thermo Fisher

- 15.12 Lock Inspection

- 15.13 Nikka Densok

- 15.14 Cassel Messtechnik

Report ID:

69

Published Date:

March 2025

Trusted by more than 10,500 organizations globally

Infaluble Methodology

Customization

Analyst Support

Targeted Market View